I guess that is what I meant by unpredictable geopolitics.

PeakOil is You

![]() by rockdoc123 » Sun 13 Jul 2014, 11:05:38

by rockdoc123 » Sun 13 Jul 2014, 11:05:38

![]() by ROCKMAN » Sun 13 Jul 2014, 16:44:05

by ROCKMAN » Sun 13 Jul 2014, 16:44:05

![]() by Graeme » Thu 11 Sep 2014, 20:46:11

by Graeme » Thu 11 Sep 2014, 20:46:11

The International Energy Agency cut its global oil demand forecasts for 2015 and said Saudi Arabia exported the least in almost three years as purchases slowed from China and Europe.

Global demand will increase by 1.2 million barrels a day, or 1.3 percent, to 93.8 million barrels a day next year, the Paris-based adviser to 29 nations said in a report today. The expansion is 165,000 barrels a day less than it predicted a month ago. Second-quarter growth in consumption slid to a 2 1/2-year low, spurring Saudi Arabia’s shipments to the lowest since September 2011.

“The recent slowdown in demand growth is nothing short of remarkable,” the IEA said. “While demand growth is still expected to gain momentum, the expected pace of recovery is now looking somewhat more subdued.”

Brent crude futures slipped below $100 a barrel this week for the first time in 14 months amid booming U.S. shale output, constrained demand and speculation that crises in Iraq, Libya and Ukraine will spare oil supplies. U.S. production is poised to hit a 45-year high next year, according to the Energy Department.

The IEA said it curbed its 2015 estimates in anticipation of weaker economic growth forecasts from the International Monetary Fund in October. Next year’s demand projections for China, the world’s second-largest oil consumer after the U.S., were cut by about 100,000 barrels a day to 10.6 million a day.

![]() by Pops » Fri 12 Sep 2014, 08:24:09

by Pops » Fri 12 Sep 2014, 08:24:09

![]() by westexas » Fri 12 Sep 2014, 08:39:12

by westexas » Fri 12 Sep 2014, 08:39:12

![]() by rdberg1957 » Sun 14 Sep 2014, 00:40:29

by rdberg1957 » Sun 14 Sep 2014, 00:40:29

![]() by JV153 » Sun 14 Sep 2014, 03:52:34

by JV153 » Sun 14 Sep 2014, 03:52:34

rdberg1957 wrote: Since randomized trials are not possible in this situation, the best option for attributing causation is looking at multiple correlations which is what I believe you are doing. In your formulation, the economic sluggishness is a result of the rise in oil prices creating a drag on the economy which then decreases demand.

![]() by ralfy » Sun 14 Sep 2014, 05:22:53

by ralfy » Sun 14 Sep 2014, 05:22:53

![]() by Pops » Sun 14 Sep 2014, 08:15:33

by Pops » Sun 14 Sep 2014, 08:15:33

rdberg1957 wrote: I'm thinking that a sign that decreased demand is due to constrained supply would be increased variability in prices. Does this make sense to you?

![]() by Synapsid » Sun 14 Sep 2014, 18:24:07

by Synapsid » Sun 14 Sep 2014, 18:24:07

![]() by Graeme » Tue 14 Oct 2014, 19:15:09

by Graeme » Tue 14 Oct 2014, 19:15:09

Demand for oil in 2015 will grow far slower than previously forecast as global economies remain weak, the International Energy Agency said on Tuesday, and prices may extend their sharp fall so long as OPEC shows no sign of countering a supply surge.

The IEA said it cut its 2015 estimate for oil demand growth by 300,000 barrels per day (bpd) from its previous forecast and now expects demand growth of 1.1 million bpd to 93.5 million. It cut its 2014 estimate by 200,000 bpd to 0.7 million bpd.

It said demand would be supported by prices near four year lows - oil LCOc1 is around $88 a barrel from above $115 in June, a 25 percent drop resulting from a boom in U.S. shale oil production, slow global growth and a strong dollar.

But it added that those low prices would remain under pressure because of supply levels: Global oil supply rose by almost 910,000 bpd in September to 93.8 million bpd, almost 2.8 million bpd higher than the previous year.

In a rare IEA comment on OPEC's strategy, its chief analyst Antoine Halff said the producer group may no longer be willing or able to adjust production as the market has been transformed by the U.S. shale oil revolution.

![]() by Tanada » Wed 15 Oct 2014, 04:15:31

by Tanada » Wed 15 Oct 2014, 04:15:31

Alfred Tennyson wrote:We are not now that strength which in old days

Moved earth and heaven, that which we are, we are;

One equal temper of heroic hearts,

Made weak by time and fate, but strong in will

To strive, to seek, to find, and not to yield.

![]() by Pops » Wed 15 Oct 2014, 09:00:26

by Pops » Wed 15 Oct 2014, 09:00:26

![]() by Graeme » Wed 15 Oct 2014, 19:11:56

by Graeme » Wed 15 Oct 2014, 19:11:56

Here we sit, inundated with gloomy but indecipherable news on the economy and energy. Perched on the cliff of a slumping global economy, the price of oil slipping down from obscene $100+ levels, the media offers massively contradictory explanations.

Do we have too much oil or too little? Is cheaper oil good or bad for the economy? Will U.S. oil production leave us a major exporter or will North American drilling rigs shut down as oil prices fall? Is Saudi Arabia’s preference for expensive oil prevailing or is it Iran in the driver’s seat seeking exorbitantly costly crude?

We should remember we’ve been here, more scarily, before. The collapse of soaring oil prices signaled the beginning of the 2008 Great Recession. This milder repeat performance is not so confusing if we look at the basics—and remember that what counts about oil is not where it is produced, or exactly how much we need, but its price.

Ten things to remember about the price of oil

1. The price for all 93 mbd (million barrels of oil a day) the world consumes are set by the cost of producing the final, most expensive marginal barrels—currently from tar sands and deep ocean drilling. That price has fallen from $110 to $90 in the last year. It’s still sky-high–triple what it was a decade ago

2. Most global oil costs much, much less than $90 to pump. Half, mostly in Russia and OPEC, cost $40 or less. Another third, conventional oil around the world and shale oil in the U.S., costs $65 or less. Only the final 10 percent requires $75 and up.

3. This gap—high consumer prices for mostly low cost oil—transfers enormous wealth from the U.S., China and Europe to the governments of Russia and OPEC. These “petroleum rents” equal 3 percent of global GDP—$2.2 trillion. They drag down the world economy as much as shutting down Great Britain. (China spends most of its huge trade surplus with the US importing oil. That’s a big reason its growth has slowed.)

The solution—and the only solution—is to break oil’s monopoly. Replacing it as a transportation fuel faster than the global economy grows, with efficient vehicles, electrification, biofuels and road to rail enables rapid growth accompanied by steadily lower oil (and fuel) costs. Our need for expensive crude will fade away.

![]() by Graeme » Thu 16 Oct 2014, 17:18:00

by Graeme » Thu 16 Oct 2014, 17:18:00

AFTER declining gradually for three months, oil prices suddenly tumbled almost $4 on October 14th alone. It was the largest single-day fall in more than a year and brought the price of Brent crude, an international benchmark, to $85 a barrel. At its peak in June, a barrel had cost $115.

Normally, falling oil prices would boost global growth. A $10-a-barrel fall in the oil price transfers around 0.5% of world GDP from oil exporters to oil importers. Consumers in importing countries are more likely to spend the money quickly than cash-rich oil exporters. By boosting spending cheaper oil therefore tends to boost global output.

This time, though, matters are less clear cut. The big economic question is whether lower prices reflect weak demand or have been caused by a surge in the supply of crude. If weak demand is the culprit, that is worrying: it suggests the oil price is a symptom of weakening growth. If the source of weakness is financial (debt overhangs and so on), then cheaper oil may not boost growth all that much: consumers may simply use the gains to pay down their debts. Indeed, in some countries, cheaper oil may even make matters worse by increasing the risk of deflation. On the other hand, if plentiful supply is driving prices down, that is potentially better news: cheaper oil should eventually boost spending in the world’s biggest economies.

![]() by Graeme » Fri 17 Oct 2014, 16:35:08

by Graeme » Fri 17 Oct 2014, 16:35:08

After four years when the highest average oil prices in history often seemed to defy economic gravity, petroleum fell in mid-2014. It had risen to $107.73 a barrel in June, even as Americans and Europeans drove fewer miles in more fuel-efficient cars, curbing consumption of gasoline, the biggest source of oil demand. Meanwhile, supply expanded as the sustained higher prices made techniques such as deepwater drilling and fracking pay off. Those fundamentals started to register in the summer, as Chinese imports sagged, Europe teetered on the brink of recession, and the stronger U.S. economy made barrels priced in dollars relatively more expensive. Instead of stanching the glut by pumping less oil, Middle East exporters engaged in a price war to defend their market share. New sources of supply such as Canadian oil sands and U.S. shale have loosened the OPEC cartel’s grip on the market. Saudi Arabia stands to gain as lower prices hurt political and economic rivals such as Russia and Iran, already facing strain from sanctions. Cheap oil also helps Saudi producers compete better against the U.S., where production costs more. In mid-October, the price dipped below $80 a barrel, testing the level at which U.S. drillers in North Dakota and Texas can still turn a profit.

The other variable, of course, is demand, and the stunning weakness this year raises long-term questions about oil’s future as consumers grow more efficient and switch to alternative fuels such as natural gas and renewable power. Oil supplied 31 percent of the world’s energy in 2012, down from 46 percent in 1973. There may come a day when oil gets cheap because it’s unwanted. That’s the argument often advanced by advocates of divestment. They warn of a financial crisis caused by a bursting “carbon bubble” of inflated energy-company valuations after fossil-fuel prices rise to account for the costs of contributing to global warming.

![]() by Pops » Sun 19 Oct 2014, 08:47:27

by Pops » Sun 19 Oct 2014, 08:47:27

![]() by Graeme » Sun 19 Oct 2014, 17:27:33

by Graeme » Sun 19 Oct 2014, 17:27:33

The recent correction in the price of crude oil should have an immediate positive impact on the US consumer as well as on a number of business sectors. However there also may be a significant economic downside to this adjustment. Here are some facts to consider.

1. The good:

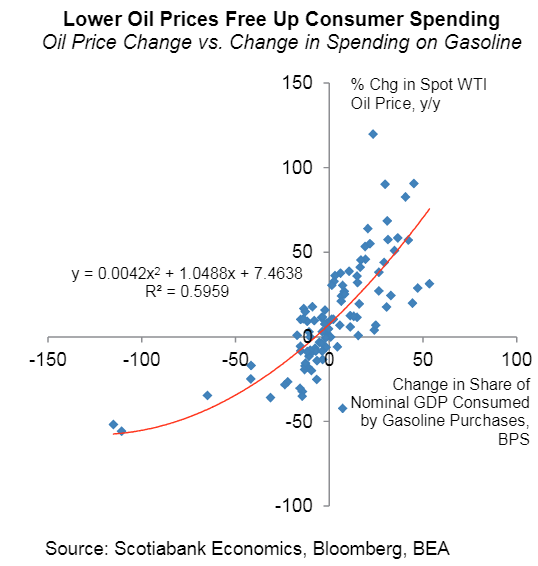

The US consumer is not only about to benefit from materially lower gasoline prices (see chart), but also from cheaper heating oil.

Furthermore, with gasoline prices lower, it is unlikely that consumers will be buying significantly more of it than they have been. Historically when oil prices fell, gasoline consumption in dollar terms also fell. Dollars saved on fuel will be redirected elsewhere in the economy.

2. The bad:

The US has become a major energy producer, with the sector partially responsible for improving economic growth and lower unemployment in recent years. As an example here is the GDP of Texas as a percentage of the US GDP. This trend is driven in part by the recent energy boom in the state.

![]() by Graeme » Mon 12 Jan 2015, 21:42:45

by Graeme » Mon 12 Jan 2015, 21:42:45

With a new report on energy decarbonization, the International Energy Agency has just made a major contribution toward implementing the greenhouse gas reduction agreements outlined at the recent UN climate negotiations in Lima (COP20). The agency, an autonomous organization, was founded after the 1970s oil crisis—a fossil fuel disaster many of us may not remember—to ensure reliable, affordable, and clean energy.

IEA’s new publication, Energy, Climate Change and Environment: 2014 Insights, sorts out current energy decarbonization policy that could help mitigate climate impacts. These include ways to accelerate decarbonization of coal-fired plants—very important in nations that are coal-rich and/or heavily invested in coal infrastructure; how to implement effective emissions trading systems; and how clean air policies can help mitigate climate change. It also updates key energy and emissions statistics at a global level and for ten world regions.

In this report, IEA ferrets out the links between air pollution policy and greenhouse gas emissions. By way of example, it shows how differently the world’s two largest emitters, China and the United States, are approaching the issue of energy decarbonization. While efforts by the Chinese to improve the poor air quality characteristic of its major cities may also help reduce GHG emissions, the nation must deliberately structure its policies to address both objectives. On the US government side, the Obama administration has at last applied longstanding air pollution regulations to target GHGs. Each country faces different challenges in fulfilling the commitments it announced in the November joint US-China climate deal and subsequently at Lima.

Access the executive summary here. The report is available in English, Japanese, and Chinese.

![]() by RepublicanfromEngland » Sun 05 Jul 2015, 18:38:55

by RepublicanfromEngland » Sun 05 Jul 2015, 18:38:55

Return to Peak oil studies, reports & models

Users browsing this forum: No registered users and 6 guests