Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on December 21, 2014

Despite Lower Crude Oil Prices, U.S. Crude Oil Production Expected to Grow in 2015

Republished December 12, 4:00 p.m. to update data.

The recent decline in crude oil prices has created the potential for weaker crude oil production. EIA’s Drilling Productivity Report (DPR) includes indicators that provide details on the effect low prices may have on tight oil production, which accounts for 56% of total U.S. oil production. Analyzing these indicators and the changes in oil production following the drop in crude oil prices during the 2008-09 recession may offer some insight into possible near-term oil production trends.

The price of West Texas Intermediate (WTI) crude oil delivered to Cushing, Oklahoma declined more than 31% from June to November 26 and another 13% after the late November announcement of the Organization of the Petroleum Exporting Countries (OPEC) decision to maintain the current production level. At $60 per barrel, the current price of oil is likely approaching or already below the expected per-barrel costs of some of the most expensive U.S. tight oil projects.

Some of the most active production fields in the country are in North Dakota. Indicators tracked by the DPR and North Dakota’s Department of Mineral Resources (DMR) cover much of the exploration and production process, from planning to production. These indicators include:

- Permits. Before drilling begins, producers must sign lease contracts and apply for permits to drill exploration and development wells.

- Rig movement. Drilling rigs must be secured and moved to permitted locations.

- Spuds. Spudding is the term for the ground-breaking process of a new drilling project. In North Dakota, the spud count is a count of new wells drilled.

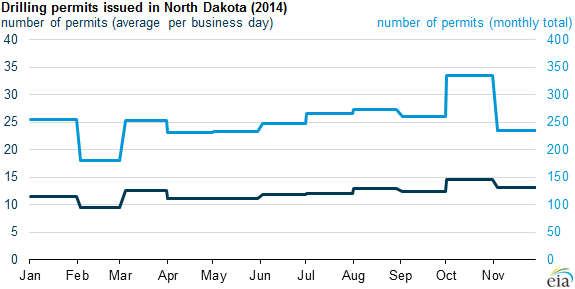

Based on the most recent data released by North Dakota’s DMR, drilling and production activities in the state have not slowed, despite the significant decline in domestic crude oil prices since July 2014. Oil production in September 2014—the latest data available—rose 5% from the prior month.

The number of permits issued in October 2014 was 28% above the September level, but it dropped 30% in November. However, when normalized based on the number of business days during those months, October is only 17% above September’s level, and November is only 10% lower than October.

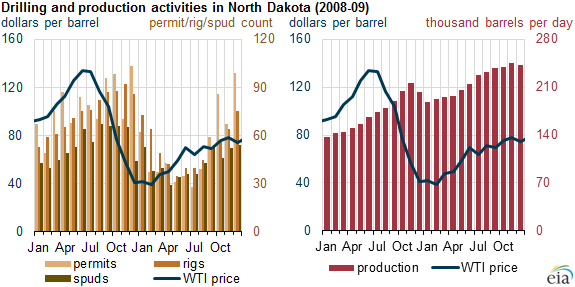

Although the current economic situation is fundamentally different from the recession of 2008-09, changes in oil prices, production indicators, and production volumes during the recession may offer insight into what may happen next with U.S. shale oil production.

During the 2008-09 recession, monthly average WTI prices fell by 71% to $39.09 per barrel between June 2008 and February 2009. At the time, shale oil production in North Dakota was still in the testing phase and thus relatively expensive. Drilling and production continued to increase until November 2008, when WTI prices dropped below $57 per barrel. Below $57 per barrel, the number of projects that were interrupted increased significantly, with the number of permits declining 73% from December 2008 to July 2009, the number of rigs declining 62% from November 2008 to May 2009, and the number of spuds declining 55% from November 2008 to April 2009. However, the decline in production was not nearly as dramatic, falling only 13% from November 2008 to January 2009, after which time production began increasing.

Looking forward, EIA expects 2015 drilling activity to decline as a result of less-attractive economic returns in some areas of both emerging and mature oil production regions. Many companies will redirect investment away from marginal exploration and research drilling and into core areas of major tight oil plays. However, projected oil prices remain high enough to support development drilling activity in the Bakken, Eagle Ford, Niobrara, and Permian Basin, which contribute the majority of U.S. oil production growth.

EIA expects U.S. crude oil production to average 9.3 million barrels per day (bbl/d) in 2015, up 0.7 million bbl/d from 2014, but down from expected growth of 0.9 million bbl/d in last month’s Short-Term Energy Outlook. However, all of the decrease in forecast production growth comes in the second half of 2015. EIA revised production growth downward by 140,000 bbl/d and 270,000 bbl/d in the third and fourth quarters, respectively, compared with the previous forecast. However, this forecast remains particularly sensitive to actual prices available at the wellhead and drilling economics that vary across regions and operators.

20 Comments on "Despite Lower Crude Oil Prices, U.S. Crude Oil Production Expected to Grow in 2015"

rockman on Sun, 21st Dec 2014 1:52 pm

This makes no sense IMHO. First, some wells producing today will either be making the same amount of oil in 2015 as they are today (very few) or they’ll be flowing at a lower rate (the vast majority). So to just keep the current US oil production rate flat thru 2015 X number of wells will have to be drilled. And if a large % of those are shale wells then X+ will have to be drilled to make up the wells that will show significant decline during 2015.

To increase the US production rate more then the X+ wells will keep it flat: Y number of additional wells will have to be drilled. And to take a guess at X and Y we need to know the future price of oil, right?

No, that’s not correct. Even if the EIA knew the price of oil down to the penny for they next few years they can’t make such a projection. As pointed out before there is no single price for oil that any trend, shale or conventional, becomes viable. Drilling decisions are made on the individual well basis: there will be Eagle Ford/Bakken wells viable at $60/bbl just as there were EFS/Bakken wells that became unattractive to drill at $75/bbl.

And the EIA has no data to determine that distribution. In fact, even the companies that have all the details the EIA will never have are going to have a difficult time culling their prospects.

And how many wells that at are viable at $$/bbl will Company XYZ drill if they lack the capex or credit line to pay the cost to drill?

Anyone can guess how many wells will be drilled in 2015 and how much oil the US producing on 1/1/2016. But no one, even the Almighty Rockman, has any credible basis to make such a prediction today. IOW the guy that wins the next lottery won’t be any better at picking numbers then anyone else. Fate just let him win. IMO the same will true for anyone’s ultimately correct prediction on future US oil production.

coffeeguyzz on Sun, 21st Dec 2014 2:32 pm

The last sentence in the next-to-last paragraph could (should?) be read and re-read by anyone who – come 12 months from now – cares to glance backwards in time and check out the predictions.

If ND oil is barely fetching 40 bucks, well, might as well go fishin’.

BUT, as they say, there is more to the story. There are about 630/650 wells in the Bak that are drilled and awaiting completion (costing 4/5 million per with the latest methods). That equates to roughly three months output.

Whiting’s recent results are extremely high – by historical standards – with their newest completion/fracturing methods having wells show 44k, 55k, and 60k barrels their first month from the same pad.

These operators (as the above article states) are able to drill/fracture multiple – 4?,6?, more? – wells on already producing pads with much lower cost (hence the description ‘development’ mode).

The current 20 buck spread ($61/$41) between Brent and ND wellhead price may prompt operators to pursue export options if both economics and the April 1, 2015 ND-mandated ‘stabilization’ procedures make sense. (Pioneer is exporting condensate under this ruling, ie. refined products = exportable).

The refrac’ing process in the Bakken is picking up steam with Marathon showing a tenfold increase in output by reentering earlier wells.

Almighty Rockman … that’s a catchy one there, Rock. Always enjoyed reading your posts going back to the numerous, gracious contributions on TOD during the Macando blowout.

Always appreciate your input/perspective, even if’n we don’t see eye to eye.

shallowsand on Sun, 21st Dec 2014 3:54 pm

Coffee. What are the well names and fields of Whiting’s wells that you cited?

coffeeguyzz on Sun, 21st Dec 2014 4:26 pm

Get back to you on that, ss. Two of the three were the NCS Multistage 94 and 104 stage fracs cuz NCS was tootin’ their horn in a Nov. press release.

The Whiting wells names were Federal something or other … will check later.

coffeeguyzz on Sun, 21st Dec 2014 5:00 pm

Shallow … Whiting O&G, permits #27520-1-2, Twin Valley Field, Lot #4, Federal 11-4TH/4HR/TFHU.

On confidential list till 4/7/15. Bruce Oksol’s blog themilliondollarway regularly has tons of current Bakken info as he is a retired Williston native with a genuine passion for this stuff.

I had almost forgotten the possibly most significant part to this … these three wells were each drilled in a SEPARATE bench, (MB, TF1, and – I think – TF2).

THAT means there may ultimately be an additional 24 or more wells on this pad. (The TF3 and 4 may yet be prospective at this location also).

Plantagenet on Sun, 21st Dec 2014 5:03 pm

The obama administration has ruled that adding a stabilizer to crude produced from cracked shales obviates the oil export ban. Since stabilizers are easy and cheap to add all US shale production is now legal to export.

coffeeguyzz on Sun, 21st Dec 2014 5:24 pm

Plant, how do you spell ka-ching?

I wouldn’t want to be selling drill mud out of Aberdeen right about now.

Plantagenet on Sun, 21st Dec 2014 5:35 pm

You’re 100% right on that coffeeguy. KSA may’ve aiming at US shales when they cut oil prices but they hit and killed the North Sea instead

Apneaman on Sun, 21st Dec 2014 6:01 pm

Looks like only a happy few will be ringing up a profit in Texass……..ka-ching-ka-ching

“Houston, You Have A Problem” – Texas Is Headed For A Recession Due To Oil Crash, JPM Warns

http://www.zerohedge.com/news/2014-12-21/houston-you-have-problem-texas-headed-recession-due-oil-crash-jpm-warns

Makati1 on Sun, 21st Dec 2014 7:31 pm

I hope oil hits $20 just to see what happens.

Plantagenet on Sun, 21st Dec 2014 8:41 pm

If Texas goes into recession can the rest of the US be far behind? Most of the GDP growth in the US over the last five years has been in Texas—-

Northwest Resident on Sun, 21st Dec 2014 9:11 pm

2015 or not, it is going to be very interesting to watch and see how certain ongoing developments play out in 2015.

Despite the brave face being put on by the shale industry, chances are their days of drilling new holes is coming to a rapid close. Credit cost has gone up significantly. With the price of oil being what it is, who will lend money on a guaranteed loss? Most likely, the shale operators will pump the holes they’ve already drilled — production will start dropping off soon enough, and that’s it. The American economy is going to get hit hard by the loss of GDP the shale industry has generated. Cracks in the illusion of BAU forever will start to form, big ones that can’t be hidden or obscured by propaganda and lies. Confidence will be shaken to the core.

In the meantime, we read that the U.K. oil industry is collapsing, we know that Russia is undergoing extreme turmoil. China is in very deep trouble and ready to implode. Japan is committing ritual economic seppuku. Venezuela and other oil producing countries are in for some real hard times once 2015 rolls around with these low and still crashing oil prices. Riots and mayhem are waiting in the wings, ready to enter the stage.

This is all coming down in 2015.

The European Union is fracturing under financial duress. In America and elsewhere, this Christmas season is likely to be the last gasp for a whole lot of retailers. Energy stocks are tanking, taking pension funds and 401Ks and everything else with them, and we don’t know how bad it is yet, but in 2015 we’ll begin to find out.

The global economy doesn’t have enough stamina left to continue pumping up the economic balloon with continued trillion$ in additional debt. And that’s ALL that has kept the global economy floating since 2008. Now we are in infinitely worse trouble than we were back in 2008. How much longer can it hold?

From my point of view, things are already crashing in slow motion. In 2015, I can’t see how the speed of collapse does NOT begin to pick up considerable speed as more dire and unsolvable energy and economic situations pile up on top of what we’ve already got going into 2015. And as it slowly dawns on people here in America and around the world that things are not good, things are most definitely getting worse and fast, and there is no glimmer of hope for the future, a broad loss of confidence could have significant implications.

I can’t imagine how TPTB will keep it all patched together for another year. They’ll try and try, no doubt, but there comes a time when you just have to admit that any further efforts to stop a raging forest fire are futile, and at that point, you grab what you can and run for your life. That moment could easily come in 2015. Maybe a little later, but my intuition tells me 2015. Let’s see if I’m right.

Nony on Sun, 21st Dec 2014 10:28 pm

Rock has a good post and I had same reaction as him (and he has good points about how fast declines are and how much is required just to keep pace). I don’t think it’s inconceivable that US production drops right away given all that. There is some “momentum” in terms of contracts existing, people finishing out plans, places where costs are half sunk (e.g. drilled wells in Bakken awaiting completion). But even so, it really does take a lot to even just KEEP PACE. So a drop right away is not at all inconceivable.

I would differ a hair with the point about inability to make a prediction. Of course we don’t know to a geometrical certitude the distribution of well potential or future price or the like. Still we can analyze the factors and make estimates. And for the wells, ND actually shares a HUGE amount of info with a basic or premium subscription. And Drilling Info has a lot of it easily searchable also.

Plant: you don’t “add a stabilizer”. This is not food additives. Stabilization is essentially light distillation if you do it a bit more, you can claim that it is processed oil. But you’re removing, not adding. And then you have two streams that have to be processed further. So it’s not an all win (consider transport being more of a pain).

CG: if it were in the economic interests to stabilize, they would already be doing it. Same as fracking. HAving it required by govt is a hindrance, not a help.

Also, the export restrictions DO have an economic impact. You can see that just from the WTI-Brent spread. It would not exist if there were no export restriction.

To me the bigger issue (not much talked about) is the hurdles and slowdowns from locations (Iowa, MN, etc.) stopping pipelines. This means instead that trains rumble which is more dangerous, less safe and worse for the environment. And it hurts production because of the added transport cost. A simple example is in McKenzie county, the Feds are stopping a one mile of NG pipeline to a processing facility. This means either large amounts of fracking or held back production in one of the sweetest areas of the Bakken.

Nony on Sun, 21st Dec 2014 11:12 pm

CG: I meant same as flaring, not same as fracking. Getting old, I guess.

bobinget on Mon, 22nd Dec 2014 8:29 am

Informative: Peak Oil Review

http://www.resilience.org/stories/2014-12-22/peak-oil-review-dec-22

Tom Whipple’s comments Dec 22, 2014

5. Quote of the Week

“[Drilling] Costs are falling nearly as fast as the price, which means oil producers can spend less to get the same or potentially even more in terms of production. While reductions in capex are coming faster than expected, it is unlikely to translate into less supply.“

— Goldman Sachs report [dartboard alert]

Nony on Mon, 22nd Dec 2014 12:15 pm

I find that hard to believe. I don’t see why costs will drop so super fast. Some of them (e.g. labor, materials that have usage elsewhere may not be so elastic). Also, in some cases, costs might already be relatively cimpetetive and not that much economic rent to be chipped away. For that matter if supply stays the same, one would expect consumption to be the same.

I guess if you posit more of an equilibrium with equal supply (rather than growth) and lower capex/drilling volume to get that…then maybe.

Kenz300 on Mon, 22nd Dec 2014 12:47 pm

Depletion rates are very high……

If new projects are put on hold…..

Nony on Mon, 22nd Dec 2014 12:50 pm

Whipple has a nice report (as always).

I think Nature screwed the pooch by using Mason Inman as their reporter. He has a very widely known background (just read up) of being a peak oil advocate of trying to find the downside of fracking, etc. Just look at some of his websites. The guy is “looking for a narrative”. Furthermore some of his early reporting on the Marcellus (from early 2014 in one of his websites) has been wrong/been abandoned…and he never finished up and said so.

Nature itself in 2011 got spanked for having advocates doing “reporting” on peak oil, shale.

Northwest Resident on Mon, 22nd Dec 2014 4:44 pm

Nony — So, fracking is all that it has been hyped up to be? Really? Next up: American energy independence?

Kenz300 on Mon, 22nd Dec 2014 7:09 pm

Sems like investments in alternative energy sources like wind and solar are a safer place to invest……