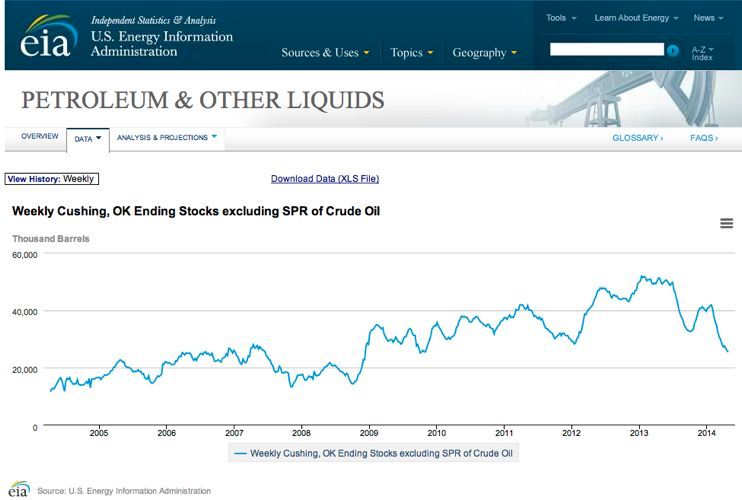

Source: EIA Cushing, OK Ending Stocks

It's been almost five years since the inventory at Cushing has been this low. Looks like Cushing peaked in Jan, 2013.

The Seaway pipeline is doing it's job...

PeakOil is You

![]() by PeakOiler » Thu 01 May 2014, 19:46:45

by PeakOiler » Thu 01 May 2014, 19:46:45

![]() by ROCKMAN » Thu 01 May 2014, 21:25:31

by ROCKMAN » Thu 01 May 2014, 21:25:31

![]() by Pops » Fri 02 May 2014, 08:21:42

by Pops » Fri 02 May 2014, 08:21:42

![]() by Tanada » Fri 02 May 2014, 08:37:49

by Tanada » Fri 02 May 2014, 08:37:49

ROCKMAN wrote:Yep. The current inventory could be emptied in less than two months. And within a month or two the parallel lines to the reversed Seaway pipeline will increase the flow from Cushing to Texas by more than 400,000 bopd. But the capacity will be needed when the other pipelines (and not the Northern leg of Keystone) underway to move production from Alberta to Cushing are completed.

Alfred Tennyson wrote:We are not now that strength which in old days

Moved earth and heaven, that which we are, we are;

One equal temper of heroic hearts,

Made weak by time and fate, but strong in will

To strive, to seek, to find, and not to yield.

![]() by Pops » Fri 02 May 2014, 09:18:00

by Pops » Fri 02 May 2014, 09:18:00

Tanada wrote:how low will inventories get and will it effect prices elsewhere in the USA?

![]() by ROCKMAN » Fri 02 May 2014, 09:42:36

by ROCKMAN » Fri 02 May 2014, 09:42:36

![]() by Pops » Fri 02 May 2014, 09:56:18

by Pops » Fri 02 May 2014, 09:56:18

![]() by westexas » Fri 02 May 2014, 10:01:00

by westexas » Fri 02 May 2014, 10:01:00

![]() by Pops » Fri 02 May 2014, 10:48:57

by Pops » Fri 02 May 2014, 10:48:57

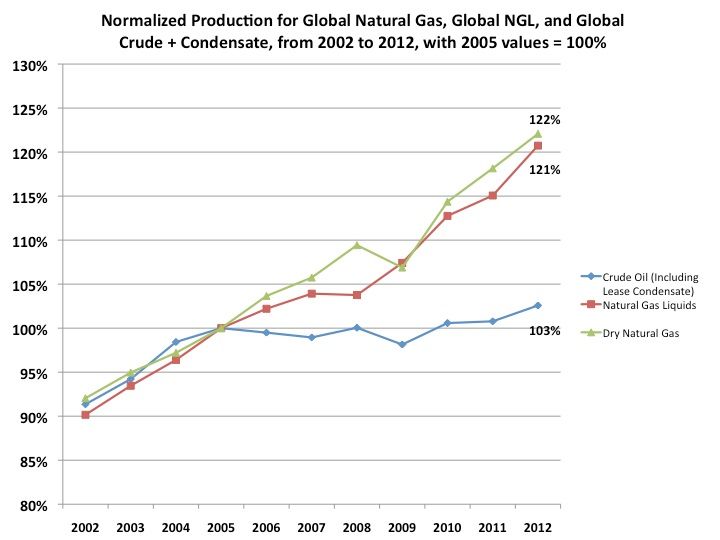

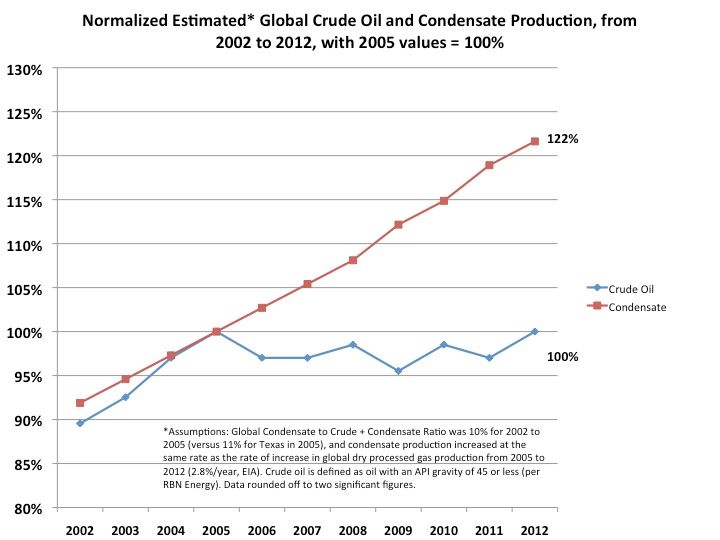

westexas wrote:I suspect that rising inventories of Crude + Condensate (C+C) mostly reflect rising inventories of condensate.

![]() by westexas » Fri 02 May 2014, 11:50:25

by westexas » Fri 02 May 2014, 11:50:25

![]() by westexas » Fri 02 May 2014, 11:52:42

by westexas » Fri 02 May 2014, 11:52:42

![]() by Pops » Sat 03 May 2014, 08:36:53

by Pops » Sat 03 May 2014, 08:36:53

Crude Oil:

A mixture of hydrocarbons that exists in the liquid phase in natural underground reservoirs and remains liquid at atmospheric pressure after passing through surface separating facilities. Crude oil may also include:

Small amounts of hydrocarbons that exist in the gaseous phase in natural underground reservoirs but are liquid at atmospheric pressure after being recovered from oil well (casinghead) gas in lease separators, and that subsequently are comingled with the crude stream without being separately measured. [lease condensate]

Lease Condensate:

A mixture consisting primarily of pentanes and heavier hydrocarbons which is recovered as a liquid from natural gas in lease separation facilities. This category excludes natural gas plant liquids, such as butane and propane, which are recovered at downstream natural gas processing plants or facilities.

![]() by westexas » Sat 03 May 2014, 10:17:58

by westexas » Sat 03 May 2014, 10:17:58

![]() by PeakOiler » Thu 12 Jun 2014, 19:57:16

by PeakOiler » Thu 12 Jun 2014, 19:57:16

![]() by vtsnowedin » Thu 12 Jun 2014, 20:34:00

by vtsnowedin » Thu 12 Jun 2014, 20:34:00

![]() by PeakOiler » Thu 12 Jun 2014, 20:46:20

by PeakOiler » Thu 12 Jun 2014, 20:46:20

![]() by ROCKMAN » Fri 13 Jun 2014, 12:04:07

by ROCKMAN » Fri 13 Jun 2014, 12:04:07

![]() by phaster » Sun 15 Jun 2014, 15:32:23

by phaster » Sun 15 Jun 2014, 15:32:23

ROCKMAN wrote:Yep. The current inventory could be emptied in less than two months. And within a month or two the parallel lines to the reversed Seaway pipeline will increase the flow from Cushing to Texas by more than 400,000 bopd. But the capacity will be needed when the other pipelines (and not the Northern leg of Keystone) underway to move production from Alberta to Cushing are completed.

![]() by ROCKMAN » Sun 15 Jun 2014, 16:12:33

by ROCKMAN » Sun 15 Jun 2014, 16:12:33

Return to Peak oil studies, reports & models

Users browsing this forum: No registered users and 8 guests