PeakOil is You

"The Shale Oil Boom" paper by Leonardo Maugeri

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Fri 18 Oct 2013, 16:31:35

by ROCKMAN » Fri 18 Oct 2013, 16:31:35

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by rockdoc123 » Fri 18 Oct 2013, 19:16:35

by rockdoc123 » Fri 18 Oct 2013, 19:16:35

CHK has been paying down their debt by liquidating assets. Last time I counted they had sold over $26 billion in assets and some of those at bargain basement prices. And last time (been a while) I saw a statement from their bankers they were only going to allow a $4 -$6 billion credit line towards their $20+ billion budget. Debt/revenue doesn't mean much if you lack enough the capital to conduct business properly.

again read their financials. Their balance sheet shows that it is a combination of very high cash flow from operations and sale of assets. Note that they have farmed down on a leveraged basis more assets than they have sold which allows them to get a piece of the production at virtually zero capex. Over the last few years they have shown positive net cash flow after taxes, debt payment etc. You portray them as a company on the edge....which they are far from. Their debt repayment schedule is laid out in a number of public documents and it is not onerous, much of it is longer term debt. There will come a point at which all of their fields are on the long flat production where they will convert the whole thing to a trust model and sit back paying opex, G&A and nothing more .....it becomes a nice cash machine. This is what potential buyers see....predictability.

Would they sell....at the right price of course

-

rockdoc123 - Expert

- Posts: 7685

- Joined: Mon 16 May 2005, 03:00:00

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by Scrub Puller » Tue 22 Oct 2013, 22:47:27

by Scrub Puller » Tue 22 Oct 2013, 22:47:27

There will come a point at which all of their fields are on the long flat production where they will convert the whole thing to a trust model and sit back paying opex, G&A and nothing more .....it becomes a nice cash machine.

For how long you reckon . . . given the nature of the assets? I thought a characteristic of their operation was (relatively) fast depletion wells. There doesn't seem to be a lot of sit-back time on that airport development.

Cheers

- Scrub Puller

- Lignite

- Posts: 296

- Joined: Sun 07 Apr 2013, 13:20:59

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by rockdoc123 » Tue 22 Oct 2013, 22:55:52

by rockdoc123 » Tue 22 Oct 2013, 22:55:52

I thought a characteristic of their operation was (relatively) fast depletion wells.

think about it, if each well has a steep decline for a couple of years or so and then levels out at a low declining rate you need a hell of a lot of wells to equal to flat production at a rate that a company might consider attractive. I'm sure they have a goal, it would be presumptuous to guess what that is.

-

rockdoc123 - Expert

- Posts: 7685

- Joined: Mon 16 May 2005, 03:00:00

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by dcoyne78 » Wed 23 Oct 2013, 11:01:21

by dcoyne78 » Wed 23 Oct 2013, 11:01:21

Several scenarios for the North Dakota Bakken/Three Forks, only TRR is considered in this chart and the middle three scenarios (TRR from 6.5 to 11.5 Gb) roughly match the April 2013 USGS TRR estimates (mean 8.5 Gb, F95 6 Gb, F5 11 Gb) for the North Dakota portion of the Bakken Three Forks play. The average new well EUR from April 2008 to Dec 2013 is 331 kb for 30 years. All scenarios in the chart assume 175 wells/month are added for 250 months for a total of 49,900 wells.

In the Chart legend the second number is the # of months from June 30, 2013 to the start of the decrease of the average new well EUR, the third number is the # of months from the start of the decrease of EUR to reaching the maximum monthly rate of decrease, and the last number is the maximum annual rate of decrease of EUR.

The chart above shows the middle (8.4 Gb) scenario from Jan 2008 to Dec 2017, the match between model and data is fairly close, though the most recent two months the data is higher than model predictions, the average new well EUR does not remain fixed but fluctuates month to month so this is expected (no model matches reality perfectly).

In a new post at my blog I present more charts and a link to some of the data in the charts and to an interactive spreadsheet that enables the user to create their own scenarios.

http://oilpeakclimate.blogspot.com/2013/10/exploring-future-bakken-decrease-in.html

Dennis

- dcoyne78

- Coal

- Posts: 476

- Joined: Thu 30 May 2013, 19:45:15

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Thu 24 Oct 2013, 09:07:30

by ROCKMAN » Thu 24 Oct 2013, 09:07:30

“Goodrich Touts Tuscaloosa Marine Success Despite Soft Shale Worries”

Bits and pieces –

First: “In fact, the company is doubling down on the Tuscaloosa after issuing 6 million shares of stock Oct. 15 to fund the accelerated drilling program in the Tuscaloosa Marine, according to a press statement”. IOW they have neither the capital nor credit capable to fund the effort. They’ve had to sell off a portion of the company to raise the capex.

Second: “Devon Energy sold its two-thirds share of 277,000 leased acres to Goodrich for $26.7 million in July, according to the companies. The price was a fraction of what equivalent acreage in the Eagle Ford formation in South Texas would go for.” The math: that’s about $145/ac. I was at Devon when they first began their Tuscaloosa run. They sold the acreage for less than 5 cents on dollar that they paid for it. And how well does Devon understand the MTS? They were one of the first players in the trend with several rigs running at the same time. Probably in excess of $100 million spent drilling.

Third: “As for the cost of acreage in the Tuscaloosa Marine, it is substantially higher than what Goodrich paid for when it bought Devon’s land, but it is substantially lower than acreage in established formations like the Eagle Ford formation, where acreage can be north of $20,000 per acre.” So Devon sold their acreage to Goodrich for substantially less than folks are paying for the rest of the acreage:”Turnham put the current market rate for acreage in the Tuscaloosa Marine Shale at close to $3,000 per acre.” So Devon sold acreage that is worth $550 million at “current market rate” for $27 million. And why did Devon give away free money??? And EFS acres going for $20,000/ac. Maybe some of it is. But one can acquire the rights to drill on 100,000 acs Shell Oil paid $1 billion for by just committing to drill a well on it. Shell has already written down $2 billion on their shale assets.

Forth: “Within the first five months of production, the Crosby well produced 100,000 barrels of oil equivalent. The total was comprised of about 1,200 barrels of oil and 600 million cubic feet of gas per day over 5 months, Turnham told Rigzone.” He can’t even see the absurdity of his own numbers. First, 1,200 bopd over 5 months is 180,000 bo. Counting NG he says it produced 100,000 boe. Which is it? Second, 600 million cu ft per day is 600,000 mcf per day. Using a price of $3.50/mcf this well, according to Mr. Turnham, the well produced over $300 million in NG alone in the first 5 months. Perhaps we should all run out and buy Goodrich stock. According to his numbers, the well paid out in several days and has in the first 5 months made about 50X the original investment.

I don’t know if Mr. Turnham is just that bad at basic arithmetic or he’s just counting on other folks not checking his numbers. The MTS may eventually prove to be viable to some degree. But I think I’ll restrain my enthusiasm until a few more wells are drilled by Goodrich beyond the first one. And then I think I’ll want to see the numbers from an outside auditor and not Mr. Turnham.

BTW I was presented with a prospect to horizontally drill and frac the MTS about 20 years ago. IOW not a new idea. Just took $100 oil to get folks to start poking holes in it.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by rockdoc123 » Thu 24 Oct 2013, 10:37:28

by rockdoc123 » Thu 24 Oct 2013, 10:37:28

First: “In fact, the company is doubling down on the Tuscaloosa after issuing 6 million shares of stock Oct. 15 to fund the accelerated drilling program in the Tuscaloosa Marine, according to a press statement”. IOW they have neither the capital nor credit capable to fund the effort. They’ve had to sell off a portion of the company to raise the capex.

How do you think small publicly traded independants finance their projects? Money doesn't grow on trees. There is only two ways through a debt instrument or through issuing equity. I know of no shareholder who has ever begrudged dilution if it allowed the company an opportunity to grow. This is SOP in the oil and gas business.

Forth: “Within the first five months of production, the Crosby well produced 100,000 barrels of oil equivalent. The total was comprised of about 1,200 barrels of oil and 600 million cubic feet of gas per day over 5 months, Turnham told Rigzone.” He can’t even see the absurdity of his own numbers. First, 1,200 bopd over 5 months is 180,000 bo. Counting NG he says it produced 100,000 boe. Which is it? Second, 600 million cu ft per day is 600,000 mcf per day. Using a price of $3.50/mcf this well, according to Mr. Turnham, the well produced over $300 million in NG alone in the first 5 months. Perhaps we should all run out and buy Goodrich stock. According to his numbers, the well paid out in several days and has in the first 5 months made about 50X the original investment.

His math on the rates is actually likely consistent. The barrels he reports are the liquid fraction of the gas and if he is speaking to measurements at the wellhead and not at the separator then 600 MMcf/d is equal to 100 boepd. At the separator the gas would be decreased at the expense of liquids but the combined fraction would equal 100 boepd minus any minor shrinkage or loss between the wellhead and separator. Note also this is very, very dry gas. 2 barrels per MMcf is not very attractive (we used to use 35 barrels per MMcf as the lower cutoff for target).

You can't use the price times the production rate to estimate value but rather have to look at the netback. $3.50 would be before all costs (capex and opex, G&A, royalties etc). My guess is that once you do that calculation the profit here is marginal as one would expect with any new shale dry gas project where there has yet been enough work done to understand efficiences.

-

rockdoc123 - Expert

- Posts: 7685

- Joined: Mon 16 May 2005, 03:00:00

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Thu 24 Oct 2013, 13:16:44

by ROCKMAN » Thu 24 Oct 2013, 13:16:44

I've had mezzanine bankers (investment companies, in reality) loan my company $120 million on less than gold plated reserves for just LIBOR +4%. Much better trade then giving up a piece of the company. Unless the company isn't worth much. Last IPO I watched first hand was Denbury Resources swapping some pretty pieces of paper to new shareholders for $260 million. And coincidentally it was to fund an EOR project in a Tuscaloosa field. Used the monies to buy the field, drilled a few wells that proved their idea wasn't worth a crap and then took a $240 million write down. The good news for Denbury management: that they didn't owe the bank one penny. In fact, they used the residual value of the field to borrow money from the bank to drill some good wells in other trends. Of course, the folks that bought the IPO shares were burned to death but, hey, you pays your money and you takes your chances. Sometimes you win big...sometimes you lose big.

600 million cu ft/day: check your decimal places. That’s 600,000 mcf/day. For folks who aren’t familiar with the oil patch a well producing 30 million cu ft of NG per day is considered outstanding. Using a 6 mcf = 1 boe conversion he’s saying the well flowed 100,000 boepd. You probably did as I did at first: read 600 mcfpd and not 600 mmcfpd. Net-back smeck-back: 600,000 mcfpd would generate $2.1 million per day gross. Do you really believe this well paid out in just a few days from the NG production alone? This has to be an absurd typo. But a typo no one involved caught because, I’ll guess, they don’t really understand the business.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by rockdoc123 » Thu 24 Oct 2013, 16:37:49

by rockdoc123 » Thu 24 Oct 2013, 16:37:49

“How do you think small publicly traded independents finance their projects?” I’ve worked or consulted for at least two dozen independent companies over the last 38 years and not one of them raised capex by issuing stock. They all used a combination of project investors, their own cash flow and credit lines. But some public companies, when their assets have little or no value to generate cash flow or don't have sufficient proved value to borrow against, have no choice but to dilute themselves by selling to folks who believe the hype about future “potential”. If the Goodrich banker believed the acreage had even a small proven potential the company is touting he would have lent them all the capex they need at a very reasonable rate.

Obviously you have never worked for a startup or low cap which I'm afraid to tell you now dominate the North American oil and gas scenario. I do not know of one single publicly traded company on the TSX that hasn't issued equity in the past 5 years. It is basically the only way to grow. As to project investors....what do you think they get for their investment? If it is a public company it is shares. As I said there are only 2 ways to raise capital if you are a public company debt and equity. The former limits your ability to get further debt and has some impact on your valuation, the latter results in shareholder dilution. As well a small company can only take on so much debt, taking debt on for exploration is stupid at best. I sit on a couple of Boards still and know how this works.

As to the Goodrich banker....what does he get in exchange for "lending". Almost always this results in a bit of carrying charges (anything from 8% normal to 13% mezzanine) and also convertible equity, which of course results in dilution. A small company doesn't have many choices and there are many, many cases of companies that have grown to a very large market cap through issuance of equity as they grow (Eg: Tourmaline and it's predecessors, Vermillion, Crescent Point, Talisman Energy, Encana, Nexen, etc etc). Find me an investor in Vermillion or Crescent Point who bemoans the dilution they experienced 5 years ago given both companies have increased their market cap immensely during that period of time.

I've had mezzanine bankers (investment companies, in reality) loan my company $120 million on less than gold plated reserves for just LIBOR +4%.

I suggest you try that in the current market. The last debt deal I saw was backed up by a 350 MM asset and the rate was 7% which is unheard of low in the past couple of years. I know of a company who last year applied for debt backed by a 30 MM USD gas plant and was quoted rates of 13% with a very onerous convert option. I have not heard of anyone in the public market getting debt in the last couple of years when it wasn't backed by proven reserves at the very least. Banks that aren't in danger of collapsing do not loan these days except on audited reserve reports or some form of hard asset they can seize in the case of default. It would be stupid to do otherwise. And as I remember you said you work for a privateco not a publicly traded company. They have leeway but at the end of the day no one is going to lend you money for nothing.

as to the math....you are correct there is mixup in wording. If you take the 100,000 boed over 5 months that equates to 4 MMcf/d I believe and the 1200 barrels of oil would be 3 bbls/Mcf which as I said would be considered quite dry. I think they meant to say about 1200 barrels of oil and 600 Mmcf of gas total over 5 months. Taking the 4 MMcf/d over 5 months you end up with 600 Mmcf so it would correct then. Reporting gas and liquids is always difficult unless you are specific. This is still a decent rate but it is almost certainly still in its steep decline phase.

-

rockdoc123 - Expert

- Posts: 7685

- Joined: Mon 16 May 2005, 03:00:00

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Sat 26 Oct 2013, 17:29:45

by ROCKMAN » Sat 26 Oct 2013, 17:29:45

But they don't tell us how they got to those numbers.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Sun 27 Oct 2013, 14:36:18

by ROCKMAN » Sun 27 Oct 2013, 14:36:18

http://seekingalpha.com/article/1777022 ... e_readmore

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by dcoyne78 » Fri 01 Nov 2013, 09:57:50

by dcoyne78 » Fri 01 Nov 2013, 09:57:50

The EIA DPR (Drilling Productivity Report) suggests that the Permian may already be near its peak,

(see http://www.eia.gov/petroleum/drilling/pdf/permian.pdf )

Maugeri suggests the Niobrara may reach about 0.5 MMb/d by 2017 which is only about 0.25 MMb/d above present levels. In the chart that follows I present some preliminary modeling on the Eagle Ford along with a Bakken scenario using fairly optimistic drilling and economic assumptions to get an ERR(economically recoverable resource) of about 13 Gb for the Bakken and Eagle Ford combined from 1953 to 2073. Peak is reached in 2016 at 3 MMb/d and decline is rapid falling below present output by 2019.

So we may see a Bakken + Eagle Ford increase of as much as 1.2 MMb/d by 2016, but 3 years later output from the EF and Bakken combined has fallen back to 1.6 MMb/d. We might also see an increase of 0.2 MMb/d by 2016 from the Niobrara play so we could see as much as a 1.4 MMb/d increase in tight oil output by 2016 (from the Bakken, Eagle Ford, and Niobrara.)

When all of the US is considered we will have the underlying decline of older wells (say about 5 MMb/d declining at 4 % per year) which amounts to 600 kb/d by 2016 and 1.1 MMb/d by 2019. So accounting for this, US output only increases by about 800 kb/d by 2016 and falls from there by 1.4 MMb/d due to the Bakken and EF decline and another 0.5 MMb/d from other US field decline to a level 1.3 MMb/d below current levels. Some of this might be offset by other tight oil plays (Granite Wash and Mississippian), but I think it is unlikely that we will be above 7.5 MMb/d of C+C output beyond 2019.

A nice discussion of the EIA's DPR can be found at http://peakoilbarrel.com/

Dennis

- dcoyne78

- Coal

- Posts: 476

- Joined: Thu 30 May 2013, 19:45:15

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Tue 07 Jan 2014, 11:51:25

by ROCKMAN » Tue 07 Jan 2014, 11:51:25

Reuters – Oil and gas producer SandRidge Energy Inc said it would sell its Gulf of Mexico operations to an affiliate of private equity firm Riverstone Holdings LLC for $750 million to focus on drilling onshore. Riverstone affiliate Fieldwood Energy LLC will also assume abandonment liabilities of $370 million. Most. SandRidge is the latest company to dispose its Gulf of Mexico assets, following Apache, Devon Energy Corp and Callon Petroleum Co. SandRidge said it would redeploy capital allocated to develop Gulf of Mexico into its mid-continent properties, including the Mississippian Oil Play of northern Oklahoma and western Kansas.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Tue 07 Jan 2014, 17:47:48

by ROCKMAN » Tue 07 Jan 2014, 17:47:48

That picture brings back a bad memory: About 20 years ago I knew a guy that lost his right arm up to the elbow doing something similar. If I were running that location he wouldn’t be doing that. More often the little things are more likely to kill you on a drill site than a blowout. About two years ago a hand probably would have taken a swing at me if I hadn’t been standing there on my “polio” crutches. He was helping to off load casing from a truck. The fork lift operator would lift it and he didn’t move away from the drop zone. I told him he needed to move back a few yards every time. He did not care for my advice. So I asked him if he had heard what happened to another hand doing exactly what he was doing just a few weeks early and about 40 miles away. That hand was crushed to death when a joint of csg rolled off the fork lift on to him. The other hand working with him knew about that accident and told him it was true. The I looked at the second hand said “So you knew about that accident and didn’t say a f*cking thing?” Now I had two roustabouts pissed off at me. But don’t bother me none. LOL.

BTW: he didn’t say thanks but he did do as I told him. Everyone hears about the big blow outs like Macondo. Almost no one outside of the oil patch hears about all the other deaths and cripplings. Also FYI: the majority of oil patch hands killed on the job die in helicopter crashes.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by TheAntiDoomer » Thu 09 Jan 2014, 10:41:18

by TheAntiDoomer » Thu 09 Jan 2014, 10:41:18

Paging Mr. Berman, Paging Mr. Arty Berman.

Do I make you Corny?

"expect 8$ gas on 08/08/08" - Prognosticator

-

TheAntiDoomer - Heavy Crude

- Posts: 1556

- Joined: Wed 18 Jun 2008, 03:00:00

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Fri 10 Jan 2014, 13:24:54

by ROCKMAN » Fri 10 Jan 2014, 13:24:54

Not sure if this is representative of the play but from one player: "The wells cost about $8.5 million each, although officials hope to reduce that by $2 million per well. The average lateral length was 5,800 feet. Those three Utica wells are out-producing the company’s first Marcellus wells, said spokesman Steven Schlotterbeck. The company has 14,000 net acres in the Utica shale." At $12,000/day gross and $8,500/day net it would take 2.6 years to pay out but only if the wells show zero decline which we know they won’t. So just like the Eagle Ford some wells (especially with higher oil yields) will be very profitable and some will be money losers. Difficult now to tell how those numbers will be split. It would also appear the Utica play is having the same problems the EFS and Bakken suffered early on: lack of NG processing infrastructure. But they continue to work on it.

Reuters - Natural gas output continued to outrun oil in Ohio's Utica shale in the third quarter of 2013, according to state data released last week from the nascent energy play. The first ever quarterly report from the Ohio Department of Natural Resources showed that 245 wells produced on average 14,500 barrels of oil per day and 370 million cubic feet of gas per day from July through September, much higher than the last recorded output from 2012. Then, oil output averaged 1,742 barrels per day and gas output was just 35 million cubic feet per day. The results are the first statewide indication of the Utica's progress since May last year when the 2012 data was released, and give an insight into an emerging boom region for gas development.

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by FrY10cK » Fri 10 Jan 2014, 14:25:16

by FrY10cK » Fri 10 Jan 2014, 14:25:16

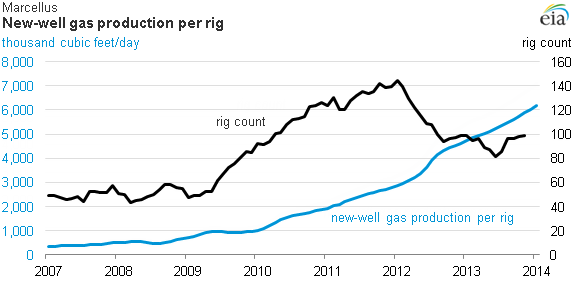

TheAntiDoomer wrote:wow, this new EIA graph speaks for itself!!

Oh! It's from the EIA! Okay then, that settles it. Peak oil was in fact, a myth.

Which one of those little smilies denotes sarcasm?

- FrY10cK

Re: "The Shale Oil Boom" paper by Leonardo Maugeri

![]() by ROCKMAN » Fri 10 Jan 2014, 16:01:11

by ROCKMAN » Fri 10 Jan 2014, 16:01:11

I don't recall anyone here or elsewhere referring to PNG so I'm a tad confused why NG production would be used as a response to any discussion about PO. Am I wrong and oes anyone here feel we're at PNG? Just seems like a pointless distraction to mix apples with zebras..

-

ROCKMAN - Expert

- Posts: 11397

- Joined: Tue 27 May 2008, 03:00:00

- Location: TEXAS

Return to Peak oil studies, reports & models

Who is online

Users browsing this forum: No registered users and 3 guests