Actually the production of "Crude Oil" isn't 3Mb/d, the production of crude

and condensate is 3Mb/d, big difference.

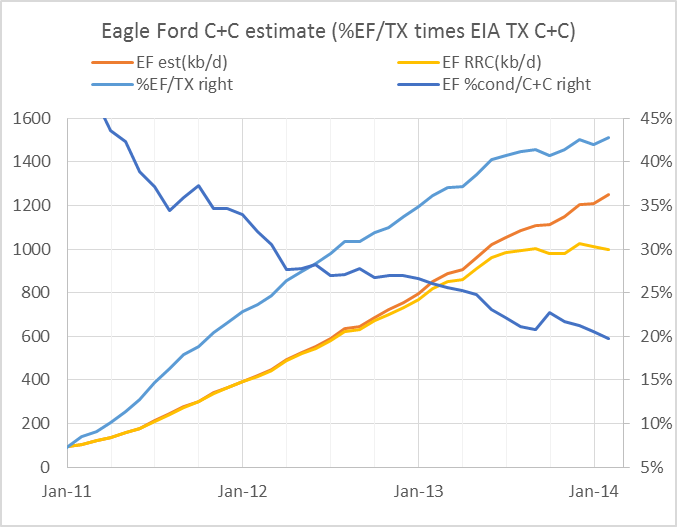

This ties in with the thread about exporting condensate, since all the increase in TX production (and all the fracked shales I guess) is essentially condensate. Condensate is light oil, naptha, natural gasoline, Coleman fuel, it is also the perfect feedstock to make plastics because it is easily (well, with lots of heat) cracked apart to make the ethylene, propylene etc that all our chachkas are made from.

From DCoyne

Here is a table from

rbnenergy.com showing just how big condensate is:

... including EOG these companies were producing between them 456 Mb/d in October 2012 and that 7 out of the 10 companies were producing condensate – a total of 319 Mb/d or 70 percent of output – leaving only 30 percent of output or 137 Mb/d as crude oil.

The companies used in the IHS survey are not named (except for EOG) but the October 2012 current production volume estimates on the chart (456 Mb/d) exceed the “official” RRC production numbers for YTD November 2012 – so the companies do represent a significant chunk of Eagle Ford production.

"Condensate" is good stuff if that's what you want, but it isn't the crude oil that the US oil biz was built around. It is very light on the API scale and while it can be made into gasoline, the refineries in the states aren't set up to refine it efficiently so it sells at a good $15-20 discount to crude oil.

--

This is important, at least to me, because I thought the reason "crude" in the Bakken was selling for such a big discount was because of transport costs, This little flap about condensate exports caused me to read up and realise that the reason for the discount is demand for condensate is lower than for crude. So lighter isn't always better.

--

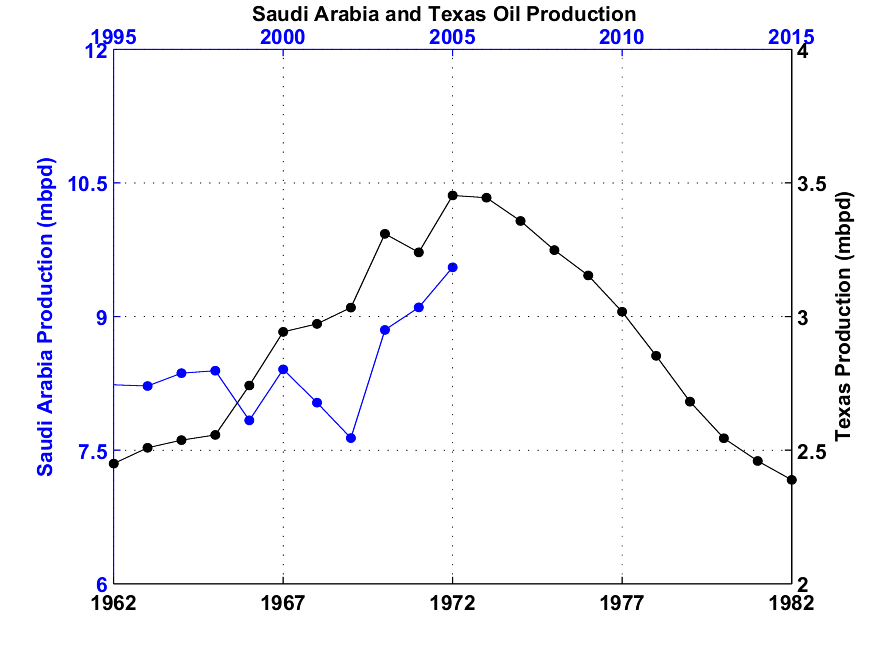

To be fair, shortonoil has been saying this for a while and so has Pstarr in his way, LOL. Westexas has also been talking about the same thing, crude oil has peaked but condensate is growing. This also relates to the chart showing the only growth in the world in US Tight Oil and the point is all the US Tight "oil" increase is condensate.

I remember talk here 7-8 years ago about the refineries in the states reconfiguring away from light oils in order to process heavy crude from KSA and canada and everyone said that was a Big Dot. It is interesting that now several Co's are frantically building "Crackers" to allow export of minimally processed condensate.

So on the one hand it is great that the drillers got something for their trillions in investment, it just wasn't what they were looking for. That of course explains why gasoline is still $3.50-$4. Naphtha makes gasoline but gasoline consumption in the US is down. We do export gasoline but global demand is for diesel and there is an oversupply of gasoline refining capacity. Refiners want to export diesel and you don't make diesel from naphtha (as far as I can tell from my wikipedia education) so they adjust their output as far as practical to make diesel rather than gasoline. The gasoline price remains high in the US.

All that explains the push to relax the rules to allow exporting condensate with little or minimal refining.

It also explains why, if there is such a glut of "crude oil" why the price of gasoline is still high. There isn't a glut of crude, it is as peaked as it ever was.

There is a glut of condensate

.

https://rbnenergy.com/imagine-there-s-n ... condensatehttps://rbnenergy.com/dont-let-your-cru ... condensatehttps://rbnenergy.com/imagine-there-s-n ... -the-worldhttp://www.digitalrefining.com/article/ ... outes.htmlThe legitimate object of government, is to do for a community of people, whatever they need to have done, but can not do, at all, or can not, so well do, for themselves -- in their separate, and individual capacities.

-- Abraham Lincoln, Fragment on Government (July 1, 1854)