A falling oil price is good for the world economyLower oil prices are not a good thing for Vladimir Putin, Russia’s president: that much is clear. But what about for everyone else? The sharp fall in crude over the past three months has produced an unusual amount of concern that, with inflation already dangerously low across much of the developed world, cheaper oil will worsen the problem.

Such fears are misplaced. To think that lower oil prices are a net negative for the world economy, and particularly for the advanced economies, is to misunderstand the problem with deflation and the cures for it.

A falling overall price level, by and of itself, is not necessarily a bad thing. China periodically slipped into deflation from the late 1990s onwards as it embarked on an extraordinary period of expansion. But with economic growth at the time at or near double-digit rates, that reflected rapid productivity growth rather than excess supply. Any slowdown in demand could easily be met by reducing interest rates.

The same is not true today for the advanced economies, particularly those within the eurozone. There, with demand too weak to match productive capacity and interest rates at or near zero, a sustained fall in the price level means that real interest rates rise. Higher real rates will encourage households further to postpone consumption and create a vicious circle of slow growth and excess capacity.

Yet while lower oil prices will have a one-off arithmetic effect on the price level and hence reduce inflation, that should boost growth rather than retarding it. Lower oil prices may hurt capital-intensive extractive industries in the medium term, but they benefit households almost immediately through cheaper petrol and other fuels. An unexpected fall in the general price level raises real incomes. This is particularly welcome in the UK, where real median household incomes last year were six per cent lower than before the global financial crisis, despite a relatively healthy economic recovery.

FTThe Guardian view on falling oil prices: mixed blessingChristmas came early for drivers this year, with a steady fall in the price at the pump of 15p a litre since the summer. Underlying the cheaper petrol is a mighty oil crash, with the price of a barrel of Brent crude near halving, from $116 in June to a mere $63 on Friday night. The frightening exposure of the big oil producers is on plain view in Russia, but – in years gone by – the oil-importing western economies as a whole would, like cheering motorists on forecourts, have regarded cheap fuel as an unalloyed boon.

This time, however, a decidedly uneasy air surrounds oil’s big dip. At first blush, this seems baffling. Oil’s ups and downs have reliably given rise to an equal and opposite swing in the mood of industry. All three late 20th-century slumps – 1974, 1980-81 and 1990-91 – followed hot on the heels of costlier crude. Less often stressed is the way that oil’s great reverses have pumped fuel into the economic engine. Britain credits (or blames) its then-chancellor’s policies for its rapid late 1980s expansion with the phrase “Lawson boom”, but the effective collapse of the Opec cartel’s discipline and the associated halving of the crude price in 1986 was just as important. For all the new-age talk about living on thin air in the late 1990s, the dotcom boom got going amid another glut of the gloop that lubricates western prosperity.

History, then, points to cheaper oil being a pedal pressed to the metal, a potential means of the world finally putting some pace into the less-than-great recovery that has followed the Great Recession. The IMF is just one voice that takes this conventional view. Optimists point to the rising role of shale gas in reducing America’s addiction to imported oil. Industry experts have been saying that shale would prove a game-changer for many years now, but – on this sunny reading – what’s recently changed is that the markets are finally paying attention. As they grasp that unpromising rocks can sometimes contain as much locked-up energy as oil wells, the perennial panic about imminent “peak” oil production recedes, and there is less reason to indulge in speculative stock-piling. Supply floods back into the market, prices drop and the economy should begin to hum.

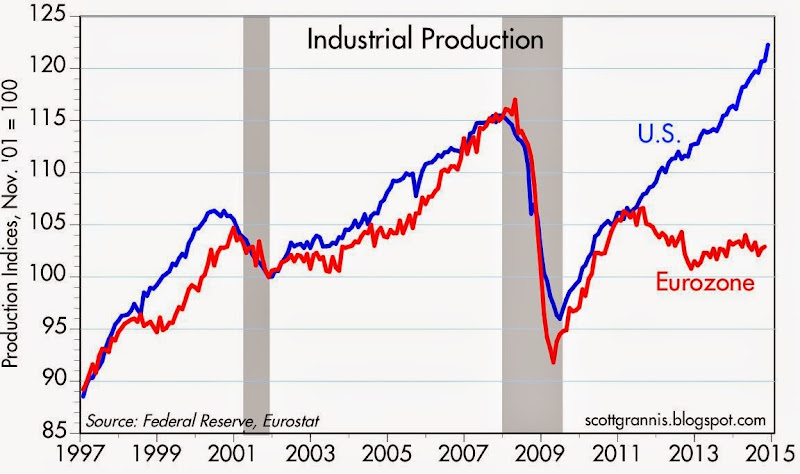

The more anxious interpretation starts by suggesting a different root cause – demand instead of supply. Oil has dipped 40%, pessimists fear, because the world no longer expects a return to economic full pelt, as that used to be understood before the crisis, nor to the growing appetite for hydrocarbons that used to go with it. Europe, Japan and – relative to its own vigorous standards – China, have all been looking anaemic this year. Like low blood pressure after a heart attack, then, cheap oil should arguably be regarded not as a sign of rude health, but rather as a consequence of malaise. In the eurozone especially, where price rises of a mere 0.3 percentage points now separate a continent and deflation, any further falls in energy costs could make the difference.

theguardian

Human history becomes more and more a race between education and catastrophe. H. G. Wells.

Fatih Birol's motto: leave oil before it leaves us.