The refinery business will come back when we work through the inventory a bit and gasoline prices are allowed to climb. Otherwise we are in for a very big wakeup call. Shutting down refineries right and left, losing refining capacity..its ok for the moment, but when we need them, where will they be? If they cant make money, they go out of business.

I guess there is some hope for demand to be low enough for that paradigm to succeed, but frankyl I doubt it, especially with any sort of economic recovery no matter how small it is.

PeakOil is You

TOD: Export Land Model

Re: The Export Land Model

![]() by AirlinePilot » Thu 04 Mar 2010, 13:17:33

by AirlinePilot » Thu 04 Mar 2010, 13:17:33

-

AirlinePilot - Moderator

- Posts: 4378

- Joined: Tue 05 Apr 2005, 03:00:00

- Location: South of Atlanta

Re: The Export Land Model

![]() by Graeme » Mon 08 Mar 2010, 22:52:58

by Graeme » Mon 08 Mar 2010, 22:52:58

Peak Oil Demand Is Coming, But Here's Why It's Not Good News

businessinsider

When oil crossed $120 a barrel for the first time in May 2008, oil cornucopians knew they were in trouble. Prices had quadrupled in just five years, yet had failed to bring new production online. Regular crude had flatlined around 74 million barrels per day (mbpd). The case for peak oil was looking stronger with every new uptick in crude futures.

The following month, prominent peak oil critic and cornucopian Daniel Yergin of IHS-CERA changed his stance: The peak oil threat would be neutralized by peak demand. Gasoline consumption had peaked in the U.S. and Europe, he argued, due to the combined effects of increasing efficiency, biofuels, and the recession.

The first was a Reuters report that the last quarter of 2009 had “wiped out” the equity of Mexican state oil monopoly Pemex, leaving it $1.4 billion in the negative. Falling crude output, falling refining margins and a burgeoning dependency of the state on its revenues had squeezed it to death.

Not only did the report offer further confirmation that the oil export crisis has arrived, but it also confirmed my growing suspicion that the oil production everyone has assumed will come online in five to ten years might, in fact, fail to materialize. Negative equity companies have a hard time raising capital for new exploration.

As we enter the post-peak phase of global oil supply sometime around 2012-2014, the price that heavily import-dependent countries like the U.S. would have to pay for that marginal barrel will become increasingly intolerable. In a weakened economy, $100 a barrel (or less) could be the new $120.

The true import of peak oil, therefore, may not be sustained high prices, but economic shrinkage. Demand will be destroyed long before oil gets to $200 a barrel, but it will not be destroyed by improved efficiency.

businessinsider

Human history becomes more and more a race between education and catastrophe. H. G. Wells.

Fatih Birol's motto: leave oil before it leaves us.

Fatih Birol's motto: leave oil before it leaves us.

-

Graeme - Fusion

- Posts: 13258

- Joined: Fri 04 Mar 2005, 04:00:00

- Location: New Zealand

Re: The Export Land Model

![]() by mcgowanjm » Tue 09 Mar 2010, 12:30:29

by mcgowanjm » Tue 09 Mar 2010, 12:30:29

AirlinePilot wrote:The refinery business will come back when we work through the inventory a bit and gasoline prices are allowed to climb. Otherwise we are in for a very big wakeup call. Shutting down refineries right and left, losing refining capacity..its ok for the moment, but when we need them, where will they be? If they cant make money, they go out of business.

I guess there is some hope for demand to be low enough for that paradigm to succeed, but frankyl I doubt it, especially with any sort of economic recovery no matter how small it is.

Refineries will/are coming back, but at the end use point:

China/India/Brazil.

Every move Hillary makes is based on that above sentence,

and she just finished the most disastrous Latin America

tour in State Dept History. And there will be no recovery-recovery to what?Hillary's Constituents:

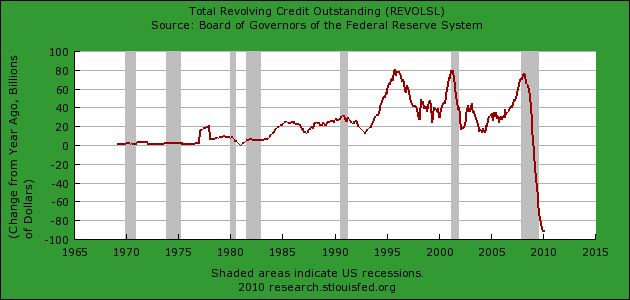

If you want to see how quickly credit is contracting take a look at this:

http://www.mybudget360.com/wp-content/u ... credit.png

- mcgowanjm

- Intermediate Crude

- Posts: 2455

- Joined: Fri 23 May 2008, 03:00:00

Re: The Export Land Model

![]() by AirlinePilot » Thu 18 Mar 2010, 14:25:24

by AirlinePilot » Thu 18 Mar 2010, 14:25:24

Chindia's Net Imports

From 2005 to 2008, Chindia's (China & India) net imports increased at about 9%/year (EIA). Expressed as a percentage of combined net exports from the (2005) top five net exporters, Chindia's net imports went from 19% in 2005 to 27% in 2008 (probably to about 33% in 2010). If we take a best case scenario for net exports from the (2005) top five and project Chindia's current rate of increase in net imports out to 2018, then in 2018, Chindia's net imports would be equivalent to 100% of projected (2005) top five net exports.

But have we ever seen a sustained near double digit rate of increase in net oil imports over a long time period?

From 1949 to 1977, the rate of increase in US net imports was 11.8%/year, exceeding the current rate of increase in Chindia's net imports. Of course, until 1973, oil prices were fairly stable and this time period (1949-1977) corresponded to generally increasing global net exports, but on the other hand Chindia has shown increasing consumption and net imports, even as oil prices rose at 20%/year from 1998 to 2008.

EIA (PDF) production, consumption, net imports chart for the US:

http://www.eia.doe.gov/emeu/aer/pdf/pages/sec5_4.pdf

Incidentally, the rate of increase in net imports from 1949 to 1970 was 11%/year, but US net imports really kicked up after US production peaked in 1970, going from 3.2 mbpd in 1970 to 8.6 mbpd in 1977 (and then entering a period of decline, before resuming the increase in later years). But in any case, the rate of increase in net imports from 1970 to 1977 was 14%/year, after US production peaked in 1970. Over the same time period, 1970 to 1977, US oil prices also rose at 14%/year (EIA).

Note that two factors contributed to the late Seventies decline in US net oil imports--falling consumption and rising production from Alaska, as the Alaskan pipeline was finished. It would appear that the all time annual record high for US net imports was in 2005, at 12.5 mbpd.

Recent EIA data show that Chinese oil production is flat, while Indian oil production is down slightly.

From 2005 to 2008, Chindia's (China & India) net imports increased at about 9%/year (EIA). Expressed as a percentage of combined net exports from the (2005) top five net exporters, Chindia's net imports went from 19% in 2005 to 27% in 2008 (probably to about 33% in 2010). If we take a best case scenario for net exports from the (2005) top five and project Chindia's current rate of increase in net imports out to 2018, then in 2018, Chindia's net imports would be equivalent to 100% of projected (2005) top five net exports.

But have we ever seen a sustained near double digit rate of increase in net oil imports over a long time period?

From 1949 to 1977, the rate of increase in US net imports was 11.8%/year, exceeding the current rate of increase in Chindia's net imports. Of course, until 1973, oil prices were fairly stable and this time period (1949-1977) corresponded to generally increasing global net exports, but on the other hand Chindia has shown increasing consumption and net imports, even as oil prices rose at 20%/year from 1998 to 2008.

EIA (PDF) production, consumption, net imports chart for the US:

http://www.eia.doe.gov/emeu/aer/pdf/pages/sec5_4.pdf

Incidentally, the rate of increase in net imports from 1949 to 1970 was 11%/year, but US net imports really kicked up after US production peaked in 1970, going from 3.2 mbpd in 1970 to 8.6 mbpd in 1977 (and then entering a period of decline, before resuming the increase in later years). But in any case, the rate of increase in net imports from 1970 to 1977 was 14%/year, after US production peaked in 1970. Over the same time period, 1970 to 1977, US oil prices also rose at 14%/year (EIA).

Note that two factors contributed to the late Seventies decline in US net oil imports--falling consumption and rising production from Alaska, as the Alaskan pipeline was finished. It would appear that the all time annual record high for US net imports was in 2005, at 12.5 mbpd.

Recent EIA data show that Chinese oil production is flat, while Indian oil production is down slightly.

-

AirlinePilot - Moderator

- Posts: 4378

- Joined: Tue 05 Apr 2005, 03:00:00

- Location: South of Atlanta

Re: The Export Land Model

![]() by TheDude » Thu 18 Mar 2010, 14:42:28

by TheDude » Thu 18 Mar 2010, 14:42:28

{kind=link}

Cogito, ergo non satis bibivi

And let me tell you something: I dig your work.

And let me tell you something: I dig your work.

-

TheDude - Expert

- Posts: 4896

- Joined: Thu 06 Apr 2006, 03:00:00

- Location: 3 miles NW of Champoeg, Republic of Cascadia

Re: The Export Land Model

![]() by AirlinePilot » Thu 18 Mar 2010, 18:42:50

by AirlinePilot » Thu 18 Mar 2010, 18:42:50

I specifically talked to Jeffrey about this and he has allowed me to post his relevant stuff right here...just so you know

-

AirlinePilot - Moderator

- Posts: 4378

- Joined: Tue 05 Apr 2005, 03:00:00

- Location: South of Atlanta

Re: The Export Land Model

![]() by TheDude » Thu 18 Mar 2010, 19:34:56

by TheDude » Thu 18 Mar 2010, 19:34:56

AirlinePilot wrote:I specifically talked to Jeffrey about this and he has allowed me to post his relevant stuff right here...just so you know

Oh great, double posting the writings of a guy who's got a problem with tautology in the first place...

Keep 'em coming, that's fine. Built up a Net Exports database yesterday from Stat Review numbers. Cripes, talk about a chore. Had to line up the same countries for Prod and Cons, make sure they're the same, erase those who weren't in both. There's a way to do this without editing that spreadsheet pros know about, I'm sure. Filters should work. Try that next time.

Top 10 Exporters 1965-2008, average YOY diff:

Mexico 25

Algeria 26

Canada 27

United Kingdom 31

Azerbaijan 32

United Arab Emirates 52

Russian Federation 53

Norway 55

Kazakhstan 56

Saudi Arabia 158

In other words, the average change year to year of Norway Net Exports over the years was 55 mb/d.

Bottom 10:

US -237

China -98

Other Europe & Eurasia -48

India -45

Venezuela -34

Other Middle East -32

Other Africa -22

Other S. & Cent. America -16

Italy -14

Indonesia -13

Thailand -10

Yeah, USA #1!!!!!!!!!!!

Also discovered that "Other Europe & Eurasia" is BP code for the USSR, by and large. Hmm, that's not very reassuring, looking at the Top 5 slackers there...

Cogito, ergo non satis bibivi

And let me tell you something: I dig your work.

And let me tell you something: I dig your work.

-

TheDude - Expert

- Posts: 4896

- Joined: Thu 06 Apr 2006, 03:00:00

- Location: 3 miles NW of Champoeg, Republic of Cascadia

Re: The Export Land Model

![]() by GoghGoner » Thu 18 Mar 2010, 20:21:03

by GoghGoner » Thu 18 Mar 2010, 20:21:03

TheDude wrote:

In other words, the average change year to year of Norway Net Exports over the years was 55 mb/d.

55 mb/d kb/d.

Interesting way to look at exports/imports -- made me realize who really upped their exports during the Seventies and Eighties. Mexico had about 30 good years. Suadi Arabia had about 40 good years

- GoghGoner

- Heavy Crude

- Posts: 1827

- Joined: Thu 10 Apr 2008, 03:00:00

- Location: Stilłwater subdivision

Re: The Export Land Model

![]() by TheDude » Thu 18 Mar 2010, 20:53:53

by TheDude » Thu 18 Mar 2010, 20:53:53

GoghGoner wrote:TheDude wrote:

In other words, the average change year to year of Norway Net Exports over the years was 55 mb/d.

55 mb/d kb/d.

Interesting way to look at exports/imports -- made me realize who really upped their exports during the Seventies and Eighties. Mexico had about 30 good years. Suadi Arabia had about 40 good years

Saudi.

Here's the whole list:

US -237

China -98

Other Europe & Eurasia -48

India -45

Venezuela -34

Other Middle East -32

Other Africa -22

Other S. & Cent. America -16

Italy -14

Indonesia -13

Thailand -10

Other Asia Pacific -7

Brazil -7

Romania -6

Peru -1

Australia -1

Egypt 1

Turkmenistan 2

Kuwait 5

Colombia 6

Denmark 7

Ecuador 7

Malaysia 7

Uzbekistan 8

Argentina 8

Iran 21

Qatar 24

Mexico 25

Algeria 26

Canada 27

United Kingdom 31

Azerbaijan 32

United Arab Emirates 52

Russian Federation 53

Norway 55

Kazakhstan 56

Saudi Arabia 158

Cogito, ergo non satis bibivi

And let me tell you something: I dig your work.

And let me tell you something: I dig your work.

-

TheDude - Expert

- Posts: 4896

- Joined: Thu 06 Apr 2006, 03:00:00

- Location: 3 miles NW of Champoeg, Republic of Cascadia

Re: The Export Land Model

![]() by truecougarblue » Thu 18 Mar 2010, 21:13:38

by truecougarblue » Thu 18 Mar 2010, 21:13:38

Dude, in your opinion which are the next five countries to slip from net exporter to net importer?

-

truecougarblue - Tar Sands

- Posts: 612

- Joined: Wed 21 Dec 2005, 04:00:00

Re: The Export Land Model

![]() by TheDude » Thu 18 Mar 2010, 23:33:58

by TheDude » Thu 18 Mar 2010, 23:33:58

truecougarblue wrote:Dude, in your opinion which are the next five countries to slip from net exporter to net importer?

Just eyeballing declines on the list I've generated, Argentina, Denmark, Egypt, Mexico, and Uzbekistan look like they're on the way out, within about 5 years max. Maybe later I'll sort out the net exporters - there aren't many - and build a chart.

Cogito, ergo non satis bibivi

And let me tell you something: I dig your work.

And let me tell you something: I dig your work.

-

TheDude - Expert

- Posts: 4896

- Joined: Thu 06 Apr 2006, 03:00:00

- Location: 3 miles NW of Champoeg, Republic of Cascadia

Re: The Export Land Model

![]() by TheAntiDoomer » Wed 31 Mar 2010, 21:25:36

by TheAntiDoomer » Wed 31 Mar 2010, 21:25:36

Someone with photoshoping capabilities should label the man in this pic Jeffrey Brown and write "Export Land Model" on the horse....

"The human ability to innovate out of a jam is profound.That’s why Darwin will always be right, and Malthus will always be wrong.” -K.R. Sridhar

Do I make you Corny?

"expect 8$ gas on 08/08/08" - Prognosticator

Do I make you Corny?

"expect 8$ gas on 08/08/08" - Prognosticator

-

TheAntiDoomer - Heavy Crude

- Posts: 1556

- Joined: Wed 18 Jun 2008, 03:00:00

Re: The Export Land Model

![]() by AirlinePilot » Thu 01 Apr 2010, 16:05:07

by AirlinePilot » Thu 01 Apr 2010, 16:05:07

Yeah so westexas is the boy who cried wolf..SO WHAT? In the near term this IS going to be the big issue. I suspect it becomes very serious after we start decline, though he seems to think its a big deal now.

This will be the main problem with which we all have to deal with due to the inability to move significantly away from the peak/plateau we are currently on. I will follow what he says far quicker than listening to corny trolls who think reserves magically grow on trees and technology always comes to the rescue.

This will be the main problem with which we all have to deal with due to the inability to move significantly away from the peak/plateau we are currently on. I will follow what he says far quicker than listening to corny trolls who think reserves magically grow on trees and technology always comes to the rescue.

-

AirlinePilot - Moderator

- Posts: 4378

- Joined: Tue 05 Apr 2005, 03:00:00

- Location: South of Atlanta

Re: The Export Land Model

![]() by AirlinePilot » Wed 17 Nov 2010, 22:18:06

by AirlinePilot » Wed 17 Nov 2010, 22:18:06

From Westexas over at TOD......

The four largest sources of imported oil into the US are Canada, Mexico, Venezuela and Saudi Arabia.

Venezuela's net exports started declining in 1998.

Mexico's net exports started declining in 2005.

Saudi Arabia's net exports started declining in 2006.

Only Canada has shown an increase, and their increase in net exports has not even been sufficient to offset the recent declines in any of the other three countries.

The four countries' combined net exports in 2005 were 14.1 mbpd, and in 2009 they were down to 11.0 mbpd--as Canadian net exports increased from 0.79 mbpd in 2005 to 1.02 mbpd in 2009 (BP). Granted, there was some level of voluntary reduction in production in Saudi Arabia in 2009, but I suspect that most of what they shut-in was what Matt Simmons characterized as "Oil stained brine," and the key point is that Saudi Arabia, Mexico and Venezuela are all showing multiyear net export declines, relative to recent peaks.

Note that the increase in US production (C+C+NGL) from 2005 to 2009 was about 0.3 mbpd (and of course 2005 was suppressed because of the hurricanes), and the increase in Canadian net oil exports from 2005 to 2009 was about 0.2 mbpd. So increased US production + increased Canadian net oil exports from 2005 to 2009 was a combined 0.5 mbpd. Over this same time frame, 2005 to 2009, combined net oil exports from Saudi Arabia, Mexico and Venezuela dropped by about 3.3 mbpd.

The four largest sources of imported oil into the US are Canada, Mexico, Venezuela and Saudi Arabia.

Venezuela's net exports started declining in 1998.

Mexico's net exports started declining in 2005.

Saudi Arabia's net exports started declining in 2006.

Only Canada has shown an increase, and their increase in net exports has not even been sufficient to offset the recent declines in any of the other three countries.

The four countries' combined net exports in 2005 were 14.1 mbpd, and in 2009 they were down to 11.0 mbpd--as Canadian net exports increased from 0.79 mbpd in 2005 to 1.02 mbpd in 2009 (BP). Granted, there was some level of voluntary reduction in production in Saudi Arabia in 2009, but I suspect that most of what they shut-in was what Matt Simmons characterized as "Oil stained brine," and the key point is that Saudi Arabia, Mexico and Venezuela are all showing multiyear net export declines, relative to recent peaks.

Note that the increase in US production (C+C+NGL) from 2005 to 2009 was about 0.3 mbpd (and of course 2005 was suppressed because of the hurricanes), and the increase in Canadian net oil exports from 2005 to 2009 was about 0.2 mbpd. So increased US production + increased Canadian net oil exports from 2005 to 2009 was a combined 0.5 mbpd. Over this same time frame, 2005 to 2009, combined net oil exports from Saudi Arabia, Mexico and Venezuela dropped by about 3.3 mbpd.

-

AirlinePilot - Moderator

- Posts: 4378

- Joined: Tue 05 Apr 2005, 03:00:00

- Location: South of Atlanta

Re: The Export Land Model

![]() by gollum » Wed 17 Nov 2010, 23:24:23

by gollum » Wed 17 Nov 2010, 23:24:23

pstarr wrote:We are still getting what we need from these four declining exporters. That tells me some country somewhere is not receiving their share. Could it be Zimbabwe? Haiti? Ireland? Portugal? Greece?

Nah. Those problems are mortgage related

We are also needing less, lots of people not going to work every day who were 3 years ago, less vacations, less air travel.

- gollum

- Heavy Crude

- Posts: 1048

- Joined: Thu 11 Nov 2004, 04:00:00

- Location: Wyoming

Return to Peak oil studies, reports & models

Who is online

Users browsing this forum: No registered users and 69 guests