Re: Baltic Dry Index Nosedive

Not coming to a store near you....

Exploring Hydrocarbon Depletion

https://peakoil.com/forums/

https://peakoil.com/forums/baltic-dry-index-nosedive-t47459-60.html

TheAntiDoomer wrote:These Shipping Stocks Have Room to Run: Maritime Expert

Imports dive at ports of Los Angeles and Long Beach

They report their worst combined import statistics in nine years for September, which is often the busiest month at the nation's biggest port complex.

LONDON — When Eastwind Maritime, a medium-size carrier company, went bankrupt this summer, few banks in the United States took notice.

The collapse of Eastwind Maritime, analysts say, while small, could well be a harbinger of more carrier failures to come.

And for Europe’s struggling banks, already plagued by a toothless economic recovery and continuing losses in real estate, the emergence of yet another questionable category of loans adds to fears that many of them are lagging their counterparts in the United States in overcoming the financial crisis.

In Britain, for example, where the economy shrank a further 0.4 percent for the third quarter, the government had to put an additional £43 billion ($71 billion) into the Royal Bank of Scotland and Lloyds, both essentially under national control, because of continuing trouble with their real estate loans.

And in Spain, where loans to companies working in the real estate sector are estimated to be almost 50 percent of gross domestic product, a consensus is growing that many banks are underreporting the value of their stricken loan portfolios.

Now there is more to worry about. Banks with large shipping industry portfolios — among them Royal Bank of Scotland and Lloyds, and HSH Nordbank and Commerzbank in Germany — could face meaningful write-downs as ship owners confront plummeting charter rates from a 25 percent drop in global trade.

But as competition for business drives cargo revenue well below what it costs to send a ship across the ocean, analysts say that ship owners may soon be the next group of borrowers unable to manage their debts.

Many see parallels to the way banks in the United States and Europe adopted an overly optimistic view of their exposure to subprime mortgages in late 2006 and early 2007.

As with Eastwind, small undercapitalized subprime lenders began to fail when home owners realized that the size of their mortgage had surpassed the value of their house, and stopped making the payments on their loans.

Although the pile of shipping industry debt does not compare to the trillions of dollars in toxic mortgage securities that infected balance sheets worldwide, the essential dynamic of plummeting ship values, burdensome debt and disappearing equity is much the same.

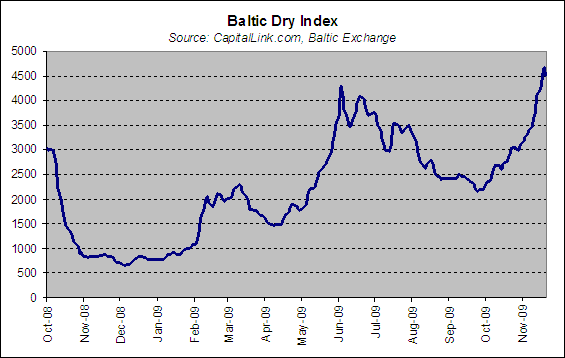

The index has been slowly recovering since it crashed to its all time low of 663 in December 2008 and has surged 32.4 per cent over the past two weeks alone.

There is also reportedly a greater interest for charters extending for several months rather than just for single voyages, as has been the case generally for this year. This suggests that shippers are confident that demand will remain stable over the fourth quarter of this year.

TheAntiDoomer wrote:Looks like the store's will be packed full of these:

Pops wrote:TheAntiDoomer wrote:These Shipping Stocks Have Room to Run: Maritime Expert

Man you really don't get it, are you sure you aren't shilling for stocks somewhere? Of course shipping stocks have room to run, they are at a third of where they were oct 07!

The BDI is at a third what it was in oct 07 - BTW it's "peak" was july of 08, not surprising since it measures the cost of shipping, not the volume.

"Oh look, a large suitcase stuffed with money, condoms, champagne and and a naked dancing girl seems to have inadvertently fallen into my lap. I'll take that down to the police station first thing in the morning, there's no point rushing down there right now, it'll be shut," said nobody to do with anything.

The Memphis Commercial Appeal on the increasingly desperate Depression picking up in the MS Delta."I've never seen a place that needed as desperately a dose of good news as this place," says Mosby, 58. Yet Issaquena and Sharkey counties aren't the only places in the Delta that are in difficult straits these days.

From Cairo, Ill., to Pointe à la Hache, La., government data make it clear that economic conditions across the Mississippi River Delta, a region already afflicted by grinding poverty and joblessness, are deteriorating. Double-digit unemployment is the norm as factories pare workers or close altogether. And the movement of Delta residents to urban centers -- including the Tennessee and Mississippi counties surrounding Memphis -- appears to be accelerating.

Ferretlover wrote:You know.... this is one of the scarier threads posted on this site......

TheAntiDoomer wrote:Yeah, it is scary how fast the BDI is recovering!Ferretlover wrote:You know.... this is one of the scarier threads posted on this site......

What amazes me most at this point is the incredible divide between USDA’s numbers and reality. The USDA is predicting record yields and production while news reports and common sense tell us that this will be the worst crop in years.

Tuesday, 18 August 2009 India: One Disaster Away From Disaster

The stalled monsoon rains this summer across large swathes of northern India are set to see rice production in the country fall from 99.15 MMT in 2008 to just 84 MMT this year, according to the USDA. [If you still have any faith in USDA estimates]

When the truth comes to light, someone at the USDA needs to pay for what has been done. The USDA’s fictitious estimates, especially for soybeans, are holding down prices and compounding the financial hardships of this miserable harvest for American farmers. The USDA’s fraudulent numbers show that the agency is aligned with Wall Street and Washington rather than America’s farmers. The USDA should be dismantled.

Mcgowan look at a longer view of the BDI, you need some perspective:mcgowanjm wrote:The BDI peak was 11 000. You're celebrating a recovery still short of 4 000. That's a dead rat(I luv cats;} bounce.What amazes me most at this point is the incredible divide between USDA’s numbers and reality. The USDA is predicting record yields and production while news reports and common sense tell us that this will be the worst crop in years.

![[smilie=5grouphug.gif]](https://peakoil.com/forums/images/smilies/5grouphug.gif "5grouphug")

So to say that 11,000 was the norm is decieving at best:

The world’s container ports industry is facing a sharp reversal in its fortunes as the sector’s first ever year-on-year fall in volumes forces an abrupt change from breakneck expansion to retrenchment.

The four biggest operators – Hong Kong’s Hutchison Ports, Singapore’s PSA, Denmark’s APM Terminals and Dubai’s DP World – have cut costs, including laying off staff, and delayed or cancelled new construction projects.

London-based Drewry Shipping Consultants forecasts a year-on-year fall of 10.3 per cent in containers moved this year, compared with 4.6 per cent growth in 1982, the previous worst year since 1956, when container shipping started.

“Before October 2008, our industry was used to 10 to 15 per cent annual growth in global trade volumes,” said Kim Fejfer, chief executive of APM Terminals.

EDITOR’S CHOICE

FT Special: Ports in a storm - Nov-26.Cranes idle in Busan’s state-of-the-art facility - Nov-26.Vulnerable Singapore reflects a picture of inactivity - Nov-26.Outlook grim for ports in southern California - Nov-26.Growth story amid trouble in the delta - Nov-26.Terminals shift towards cost containment - Nov-26..“Not only are we in the middle of a volume crisis but our customers, the container carriers, are in an even more difficult situation because of the over-capacity in that particular sector,” he added.

Mohammed Sharaf, chief executive of DP World, said the industry was facing a major change. “We have to shift gears, shift our thinking process to meet the demand.”

The slowdown has increased the focus on cost-cutting. “We have more time to focus on specific areas such as efficiencies of the equipment, the utilisation of the equipment and the challenge of shuffling man hours,” Mr Sharaf said. All the big four operators, except DP World, have cancelled port projects.

Hutchison has pulled out of projects in Thessaloniki in Greece and Manta in Ecuador, although it insisted both were a result of efforts by the authorities to make unilateral changes to its contract.

PSA is known to have cancelled some projects, but declines to comment publicly.

Mr Fejfer confirmed that APM Terminals had pulled out of some projects but declined to say which. “On some projects, we had to review the proposition from a cost point of view and a capital expenditure point of view,” he said. “We also unfortunately had to cancel a few projects.”

Neil Davidson, ports analyst at Drewry Shipping Consultants, said that, while terminal operators had suffered falling revenue, their profit margins were “largely unchanged”.

Mr Sharaf said he believed the downturn could prove ultimately healthy for operators if it helped them to learn to control costs better. “I think this is something good which is happening, in a way,” he said.

eXpat wrote:The world’s container ports industry . . .

A new report by VoxEU provides some detailed perspectives on just how bad the collapse in world trade has been as a result of the last year's events. In a nutshell: the current Great Recession/Depression has plunged the world into an unprecedented collapse of global trade, with the resultant blowing of liquidity bubbles having been the only way for individual governments to respond to this massive loss of GDP. And while drops in world trade are nothing new, with a 5% drop in the 1982 and 2001 periods, as well as a more severe 11% contraction in the 1970s, the current plunge of over 15% YoY is truly unprecedented and demonstrates the fragile nature of "globalization." What the outcome of this fact will be, depends entirely on the traditional dynamo of world economic growth - the US consumer, and unfortunately he is still down for the count.

From the VoxEU report:

Global trade has dropped before ? three times since WWII ? but this is by far the largest. As Figure 1 shows, global trade fell for at least three quarters during three of the worldwide recessions that have occurred since 1965 ? the oil-shock recession of 1974-75, the inflation-defeating recession of 1982-83, and the Tech-Wreck recession of 2001-02. Specifically:

* The 1982 and 2001 drops were comparatively mild, with growth from the previous year’s quarter reaching -5% at the most.

* The 1970s event was twice that size, with growth stumbling to -11%.

* Today's collapse is much worse; for two quarters in a row, world trade flows have been 15% below their previous year levels.

Shipping costs rebounded this year, after plunging a record 92 percent last year, as the global economy recovered from its deepest recession since World War II. China, the world’s biggest consumer of iron ore and coal, spent $586 billion to stimulate its economy. The two commodities are the biggest cargoes carried by ships included in the Baltic Dry Index.

“Next year is going to be a better year than a lot of people expect, but a lot depends on Chinese demand continuing,” said Michael Gaylard, strategic director at Freight Investor Services Ltd., a London-based derivatives broker.