The energy transition is driving the next commodity supercycle, with immense prospects for technology manufacturers, energy traders, and investors. The transition from ICEs to EVs has become a focal point of the global electrification drive. In 2020, global sales of EVs increased a robust 39% year on year to 3.1 million units, an impressive feat right in the midst of a major health crisis. 2021 is "yet another record year for EV sales globally," with an estimated 5.6 million units sold, good for 83% Y/Y growth and a 168% increase over 2019 sales. BNEF has forecast that annual EV sales will approach 30 million units globally by 2030(the

Global Automotive Market consisted of 85.32 million units in 2020, and is expected to reach 122.83 million units by 2030).

That means that the world will need a massive ramp up in electric battery production. Indeed, DOE says the worldwide lithium battery market is expected to grow by a factor of 5 to 10 in the next decade. Luckily, the United States appears to be up to the task. According to the U.S. Department of Energy, 13 new battery cell gigafactories are expected to come online in the U.S. by 2025. Apart from Tesla Inc.'s new 'Gigafactory Texas' in Austin, Ford Motors has lined up three gigafactories; one in Northeast of Memphis, TN, and two in Central KY. General Motors plans to build no less than four gigafactories. Meanwhile, SK Innovations plans to build two battery factories in Northeast of Atlanta, GA. Stellantis is teaming up with LG Energy Solution and Samsung SDI to build two factories in yet to be determined locations while Toyota and Volkswagen plan to build a gigafactory apiece.

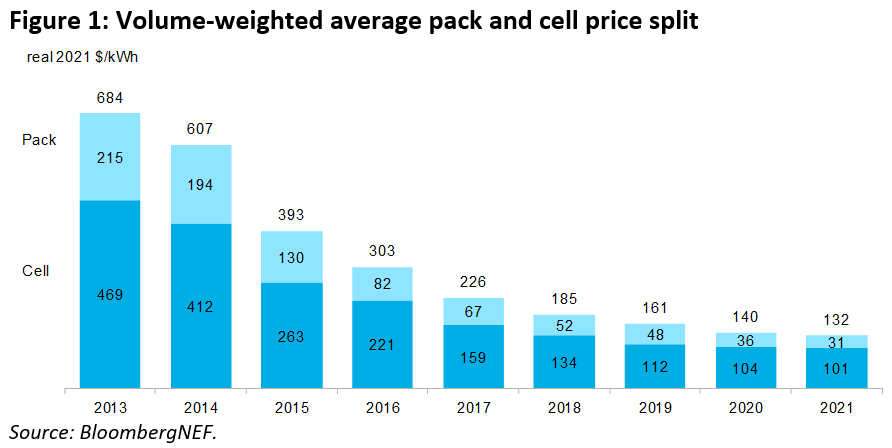

At the center of our green energy drive are solar and wind power, both of which are expected to contribute nearly half of the global power mix by 2050 as per Bloomberg New Energy Finance. The intermittent nature of these renewable sources, however, means that large-scale storage is absolutely critical if the world is to successfully shift away from high dependence on fossil fuels. The surge in lithium-ion battery production since 2010 can be chalked up to huge improvements in the technology from a cost and performance standpoint.

Over the past decade, an 85% decline in prices fueled a revolution in lithium-ion battery technology, making electric vehicles and large-scale commercial battery deployments a reality for the first time in history. The next decade will be defined by a massive increase in utility-scale storage. According to the EIA, operating utility-scale battery storage power capacity in the United States more than quadrupled from 2014 (214 MW) through March 2019 (899 MW). The organization projects that utility-scale battery storage power capacity could exceed 2,500 MW by 2023, or a 180% increase.

Battery Metals Demand ExplodesBy 2030, consumption of lithium and nickel by the battery sector will be at least 5x current levels while demand for cobalt, used in many battery types, will jump by about 70%. Meanwhile, diverse EV and battery commodities such as copper, manganese, iron, phosphorus, and graphite—all needed in clean energy technologies and to expand electricity grids—will see sharp spikes in demand.

According to the analysts, in a net-zero emissions scenario, the metals demand boom could lead to a more than fourfold increase in the value of metals production–totaling $13 trillion accumulated over the next two decades for the four metals alone. This could rival the estimated value of oil production in a net-zero emissions scenario over that same period, making the four metals macro-relevant for inflation, trade, and output, and provide significant windfalls to commodity producers.

{kind=link}