Ron Muhlenkamp is the founder and portfolio manager of Muhlenkamp & Co. Inc., established in 1977 to manage private accounts for individuals and institutions. In 1988, the company launched a no-load mutual fund as an investment vehicle for all investors, large or small. Muhlenkamp is an award-winning investment manager, frequent guest of the media, and featured speaker at investment shows nationwide. His work since 1968 has been focused on extensive studies of investment management philosophies, both fundamental and technical. In addition to publishing his quarterly newsletter, Muhlenkamp Memorandum, he is the author of “Ron’s Road to Wealth: Insights for the Curious Investor.” Muhlenkamp received a bachelor’s degree in engineering from M.I.T. in 1966, and a master’s degree in business administration from the Harvard Business School in 1968. He holds a Chartered Financial Analyst (CFA) designation.

The Energy Report: Ron, in an online seminar in June, you compared the government’s response to the 2008 financial panic and recession with its response to the recession of 1980–82. How are those recessions comparable?

Ronald Muhlenkamp: We’ve had 12 recessions since World War II. We had a serious recession in 1973–74, and I’ve done a lot of work on recessions ever since. The 2008 recession shared a distinction with the 1980–82 recession: Each, at the time, was the most serious recession since the Great Depression of the 1930s. Each was preceded by conscious government policies that were meant to improve the economy. In the 1970s, we printed money in an attempt to negate periodic recession. We got inflation. In the early 2000s, we encouraged—mandated—the writing of mortgages to people with low incomes. We got a housing bubble. We then responded to these two recessions with very different policies, and the policies have produced different results. It is important for us to learn from that.

The 1980–82 recession followed a decade of high inflation during which an accommodative Federal Reserve was printing money. By 1979 inflation had reached 13%, and most economists believed it was intractable, that it was going to be 10% or more going forward.

Jimmy Carter appointed Paul Volcker chairman of the Federal Reserve, and Volcker said he was going to break the back of inflation by printing money at a 6% rate. Conventional economists responded by saying, “If inflation is 10% and you print money at only 6%, you’ll have a minus-4% real gross domestic product, and you’ll have a very serious recession bordering on depression.” Volcker said, “I’m going to do it anyway.” Within three years, inflation went from 13% to 3%.

Many economists argued at the time that the U.S. was a slow-growing economy; that the economy was mature, and the like. What Volcker and, later, Ronald Reagan, proved is that bad policy caused the distortion. The first part of the solution was Volcker saying, “I’m going to restrict the growth of the money supply.” The dollar was weak, which is why Carter appointed him. What Volcker proved is that real growth under proper policies is stronger than inflation; that you could, in fact, lick inflation by restricting the growth of the money supply.

“It’s far more expensive to hire someone today than it was back in 1996, or in 2006. We believe that is why employment growth in the latest expansion has been so slow.”

When Reagan was elected, we were in recession. To get the economy going again, he removed some of the burden from the employers and the general public by cutting tax rates and regulations. He essentially viewed the employer as a partner with government in getting people back to work. I refer to this period as the first great economic experiment of my adult lifetime.

The economic forecasts from the 1970s all predicted continued low growth and high inflation. Reagan and Volcker changed policies, and what we got was low inflation and high growth through the 1980s and the 1990s. That was the first great experiment: These two men led a change in monetary policy and fiscal policy that gave us good growth for a generation.

I think the reason the 2008 recession was so serious was that in 2005 and 2006, the Fed was raising interest rates and tightening monetary policy a little bit, but stopped short of triggering a recession. Every recession since World War II has been triggered by—not necessarily caused by—the Fed raising interest rates. This time, it raised the rates but stopped at 5.25%, trying to get a soft landing.

Behind that, it was mandated that if you wanted to be in the mortgage brokerage business, you had to make more loans to people with low incomes. The Fed accommodated this with monetary policy, and accountants instituted a mark-to-market rule on asset holdings, including for regulatory purposes, banks and insurance companies. In 2007 and 2008, as the price of bonds came down, banks and insurance companies, by regulation, had to either raise more equity capital or sell off their bonds. Of course, in selling their bonds, they drove the prices even lower.

We think the recession ended up being deeper and longer than it would have been without these two changes. In the middle of the 2008 recession, and coming out of it, the Fed continued to print money. The government also told employers that regulations were going up, their taxes were going up, and that they were going to have to pay for increased prices on healthcare.

In our latest newsletter (Muhlenkamp Memorandum #111), we show what employment costs have done. In January of every year, every one of our employees gets a W-2 form that shows that employee’s gross pay, deductions, and net pay. We also give them a statement showing the employee cost to the company, including FICA and health insurance. Ignoring pension and profit sharing, in 1996, just the mandated taxes and contributions to Social Security, plus healthcare insurance for employees, cost the employer $1.53 for every $1 an employee took home. In 2014, that ratio is $1.94 to the employer per take-home $1. Employer costs have gone up $0.41 (which is 27%). Most of that has been in healthcare costs, but the point is that it’s there.

It’s far more expensive to hire someone today than it was back in 1996, or in 2006. We believe that is why employment growth in the latest expansion has been so slow. As employers, we know healthcare costs are going up and insurance costs are going up, but we don’t know by how much. We’ve been promised that our taxes are going up. The same is absolutely true of regulation. Half of the Dodd-Frank rules haven’t been published yet. We know there are more rules coming.

“We are seeing what happens when, coming out of a recession, you flood the economy with money and promise employers that their costs are going up.”

The 1980–82 recession was the first great economic experiment; I call 2008 the second great economic experiment. We are seeing what happens when, coming out of a recession, you flood the economy with money and promise employers that their costs are going up. What we’ve seen is a subpar response. We have seen about 2% growth coming out of this recession. There was never really a catch-up. Of course, the population grows about 1%, and, historically, we’ve gotten about 2% productivity. This time, we’re getting about 1% productivity. The data is out there for those who choose to look.

Our company just got the bill for our health insurance for next year, and the quote is up 19%. Our taxes are going up and we know more Dodd-Frank regulations are coming. As a businessman and an employer, it’s very hard for me to justify hiring people or putting money out for capital expenditures when these increasing costs have been promised.

TER: Which specific metrics in the two recessions are directly comparable?

RM: Many recessions aren’t visible in consumer spending. The consumer cuts back on long-term stuff, like housing and autos; those are cyclical purchases. But people don’t cut back on food. They don’t cut back on what they spend for utilities; they still heat their houses.

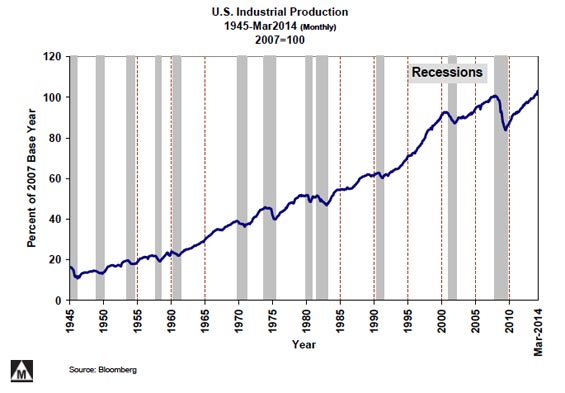

Most recessions are inventory and capital expenditure recessions. Industrial production always cuts back. These factors are common to all recessions, though each recession had certain characteristics that have allowed us to do pretty well in the investing market place for 30 years. Each looks just different enough that people can say it’s different this time. But the underlying pattern looks pretty much the same.

What made 1980 look different was the backdrop of high inflation. What made 2008 look different was the focus on encouraging people to borrow money and buy houses. The public made the house prices go up, while the Federal Reserve was keeping interest rates low. The Department of Housing and Urban Development mandated more mortgages to people in low-income brackets. What we found was that if people bought a house with no money down, they had no stake in it, and they were willing to default and walk away. People didn’t do that when to buy a house they had to put 10–20% down. They had a stake in it.

We used to believe that recessions occurred every three to five years, because in the 1950s and 1970s, they did. When John Kennedy lowered taxes in the 1960s, we got nearly a decade between recessions. Then, in the 1980s and 1990s, we went a longer period of time without a downturn, which I think was due to the success of the response to 1980 policy changes.

TER: How is the Muhlenkamp Fund doing this year?

RM: Through June we were up about 5%. We’re just a bit behind the Standard & Poor’s 500 Index.

We got hit in 2008. I misjudged the amount of damage that mark-to-market and other changes would bring. I expected the Fed to act differently than it did. We went back and took a look at what happened, and as a result we’ve added “who might have to sell and how much” to our checklist.

Normally, hedge funds have to sell any time the market comes down, because they’re on leverage. What we got in 2008 were banks and insurance companies that were forced to sell bonds because of the mark-to-market standard of accounting—which, incidentally, the Financial Accounting Standards Board (FASB) quit enforcing in March 2009. I don’t know if the rules have been taken off the books yet, but the FASB said, in response to a congressional committee, that it was not going to enforce these rules, and that became the bottom of the market.

TER: What is the Fed’s retreat from quantitative easing (QE) doing to your investment strategy?

RM: We think that’s a move toward normal, which is always good. As a country, we’ve tried to adjust for poor fiscal policy with monetary policy. The biggest bubble out there is in low-level, short-term interest rates. The Fed says it sees no bubble, but the Fed’s causing a major one. The premise was that low interest rates would help people buy houses and encourage companies to build factories. Neither of those is happening, even at normal levels.

“The biggest bubble out there is in low-level, short-term interest rates.”

What has happened is retirees trying to live on interest are getting no income. Retirees and pension funds are being squeezed big time. And the reason people aren’t buying houses is that they overbought 10 years ago, and they no longer believe housing always goes up. The fact that they can get a cheaper interest rate is not enough, because their perception of the asset has changed. Companies aren’t building plants either. They don’t know what the rules are. Even if you can borrow money at 3% instead of 6%, if you don’t see demand for the plant and don’t know what the rules will be, you’re not going to build it.

The Fed set out to get employment up and the economy going. That hasn’t happened—but it did help get the stock market up. If the Fed had said four years ago its goal was to get the stock market up, it would have been shot down politically. What (Fed chairwoman) Janet Yellen basically said a couple weeks ago was that the Fed would continue to keep interest rates low because it hasn’t worked. She would say it hasn’t worked yet, but I would say it hasn’t worked.

Ending QE3 is a move toward normalcy, but it’s simply not enough. The best thing you can do for retirees is to allow the return on their savings to go from zero in treasuries or less than 1% on a certificate of deposit back to 2–3%. If that happened, retirees would be more confident, and it would also take some of the pressure off the pension funds.

TER: You have only a couple of energy companies in your Top 20. Are you planning to keep that ratio?

RM: Our Top 20 are the companies that have done well for us. In energy we have one foot in a half-dozen different places. We own a couple of exploration and production companies but are not concentrated on any given one. We own some service companies. Halliburton Co. (HAL:NYSE) shows up in our Top 20. We own a number of companies that we think benefit from cheap energy.

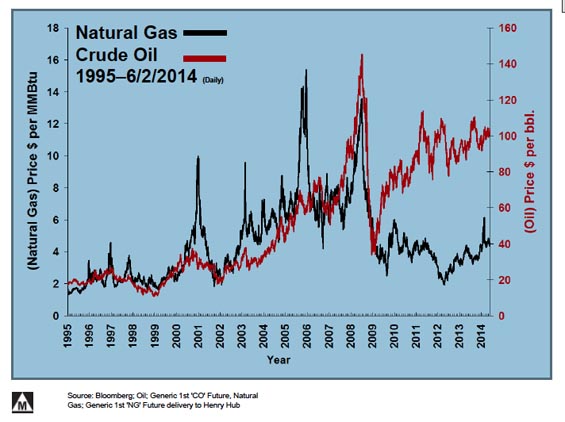

Natural gas now sells for less than half, on a British thermal unit (Btu) basis, of what crude oil sells for. That’s going to draw people to use natural gas. We own stock in companies that convert engines from diesel to natural gas, for both the original equipment manufacturers (OEM) and the aftermarket.

I believe the big driver is the relative cost of energy. We have investments in a number of companies that, individually, look fairly small. But in the aggregate we have a pretty good bet on the amount of energy used.

“We believe we’re in the process of cutting the cost of energy in this country in half in the current decade.”

We’re betting that people will use more natural gas. At $3/thousand cubic feet ($3/Mcf) for gas, it becomes competitive with coal. So we don’t think the price will go much below $3/Mcf, because at that point people who now use coal will convert to natural gas. We don’t think the gas price will get much above $5/Mcf because a whole lot of gas is profitable to drill at $5.

I live north of Pittsburgh in Butler County, Pennsylvania, which sits on top of the Marcellus Shale. Right now, the spot price on Marcellus is well below $3/Mcf. For the next year or two, we think the price will be on the low side of $4/Mcf. But what we’re trying to bet on are the people who will end up using more gas and the people who facilitate that as the price stays well below crude oil.

TER: The forward price for natural gas, at least on the NYMEX, is below $4/million Btu ($4/MMBtu; equivalent to $4/Mcf).

RM: But that’s a nationwide price. Some of the quotes on the spot price in the Marcellus are $1.50/Mcf. That makes sense as a spot price, but in Massachusetts, we’re seeing spot prices of $7–8/Mcf. It’s cheap in Pennsylvania and expensive in Massachusetts, because there isn’t enough pipeline to meet demand between the two. Of course, they’re still flaring gas in Williston, North Dakota, in the Bakken field, which basically means that it’s free, because there isn’t enough pipeline to ship the gas even to places like Minneapolis, St. Paul or Chicago.

Nationwide in the U.S., the price is about $4/Mcf. In Europe, it’s $12/Mcf and in Japan, it’s $16/Mcf, which is driving the move toward liquefied natural gas (LNG) terminals and LNG tankers. We’ve been asking people for years what it costs to take natural gas, compress it, liquefy it, ship it and then regasify it. That number has been about $6/Mcf. It may, over time, work its way down to $5/Mcf. But if we have gas at $4/Mcf and Japan is paying $16/Mcf, that’s what is driving the LNG focus.

TER: Is the gas in storage being replenished fast enough to restrain the price spikes coming next winter?

RM: We can get numbers on this weekly. We’re still running below normal in storage, and we’re not gaining much. If nothing else hits the fan, it looks like we might just make it.

Two years ago, when we had a warm winter, gas fell to $2/Mcf in April 2012. This last year we had a cold winter, and fuels like propane were on allocation in Ohio, Indiana and various places. If we have a normal winter, we may get through it OK, but we don’t have a cushion. There are a lot of moving parts here. It’s going to be interesting to see how all this shakes out.

TER: You mentioned Halliburton, which reported great results for Q2/14. What sparked that growth?

RM: Part of it is the return to demand for fracking. The drillers are telling us that to the extent they can put more sand into the formation—and they usually do that by shortening the segments when they frack it—if a given well is fracked in a few more stages, and more sand is put into each, it more than pays in terms of the amount of gas that comes out of the well. This year has been a very good year for the fracking companies. Halliburton is the biggest but, of course, it does a lot of other things as well. The company is a class act in many ways, but we think it has been helped this year by the increased demand for fracking.

TER: Any other energy companies on your Top 20 list that you want to talk about?

RM: Rex Energy Corp. (REXX:NASDAQ) is also in our Top 20. I have two farms in Butler County that the company has leased to drill. Rex just brought on a processing plant, which allows it to up volume significantly this year, on the order of 40–50%. The company continues to improve its economics in the drilling of wells. Most of the drilling stocks have come down in the last month or so, as the spot price of gas has come down. That makes sense, but the spot price for gas is getting low enough. At these levels, Rex is a great play. [Editor’s note: Since this interview was conducted, Rex Energy nearly tripled its Marcellus acreage in a transaction with Royal Dutch Shell Plc (RDS.A:NYSE; RDS.B:NYSE).]

TER: It looks like Rex is very near its 52-week low. Is that a bargain or is that a warning?

RM: I think it’s a bargain. The stock has come down as the spot price for gas in Appalachia, in the Marcellus, has come down. We’ve seen daily spot prices at $1.50/Mcf. I don’t think spot prices will stay low very long. The Environmental Protection Agency continues to put pressure on electric utilities to switch from coal to something cleaner, like gas. I think gas is the best alternative. And we think Rex is at a bargain price.

TER: Is there another company you’d like to mention?

RM: Westport Innovations Inc. (WPT:TSX; WPRT:NASDAQ) has a joint venture with Cummins Inc. to make diesel engines, primarily for OEM. We think the next big thing is conversion of over-the-road diesel trucks to natural gas. It’s taken a little longer than we thought, but providing natural gas at stations nationwide is the next logical step. Clean Energy Fuels Corp. (CLNE:NASDAQ) is the 800-pound gorilla in terms of the service stations.

Cummins Westport is the big guy in terms of converting OEM trucks. The service stations weren’t in place a year ago; they now are. The 12-liter truck engines weren’t available a year ago; they now are. We’re sizable investors in what we think will be a changeover. It won’t be 100%, but it will be significant.

You may recall that in the 1950s, nearly all over-the-road trucks burned gasoline because diesel engines were hard to start. The same was true for farm tractors. But once people figured out how to make diesel engines easy to start, over-the-road trucks switched from gasoline to diesel in less than a decade. A similar changeover is happening with railroads. The head of Burlington Northern Santa Fe LLC (BNI:NYSE) has said that the company is testing switching from diesel to natural gas. He was quoted as saying that it might be the biggest change in railroading since the switch from steam to diesel. Frankly, I don’t think it will be quite that big, but the largest single user of diesel fuel in the country is Burlington Northern.

We believe we’re in the process of cutting the cost of energy in this country in half in the current decade. It’s already happened for consumers who heat with natural gas, but almost no one is aware of it. When you cut the cost of energy in half, amazing things happen in an economy. We’re still only beginning to see the effects of cheap natural gas on the U.S. economy. We’re trying to find different ways to play that, because we’re not quite sure which companies will be the winners.

TER: Do you issue ratings for your companies?

RM: As investors, we don’t publish research. We do our own research for our own purposes. In fact, if we think we have an edge, we don’t talk about it until we’re done buying it. At current prices, my appetite is bigger than it was six months ago. We think having energy priced at two different levels, crude oil being over twice the price of natural gas, has created too wide a spread for energy consumers not to try to shift from one to the other. We’re trying to play every which way we can to benefit from the shift from crude oil to natural gas.

TER: I appreciate your time.

RM: It’s been a pleasure.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Tom Armistead conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor. He owns, or his family owns, shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of Streetwise Reports: None. Streetwise Reports does not accept stock in exchange for its services.

3) Ronald Muhlenkamp: I own, or my family owns, shares of the following companies mentioned in this interview: Halliburton Co., Rex Energy Corp., Westport Innovations Inc., and Clean Energy Fuels Corp. I personally am, or my family is, paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

( Companies Mentioned: HAL:NYSE, REXX:NASDAQ, WPT:TSX; WPRT:NASDAQ, )

paulo1 on Sat, 30th Aug 2014 11:20 am

re:

“We believe we’re in the process of cutting the cost of energy in this country in half in the current decade.”

And the IEA expects Bakken to peak in 2016? Others in 2015, and some say the increasing decline rate and lack of replacement indicates a slowing is starting right now. Current decade is almost 1/2 over if you call it 2010-2020. If you call it 2014-2024….or 2008-2018 which is a big focus on this article, namely, how is recovery developing after the 2008 downturn considering we are just over 60% through this 10 year cycle?

And if NG exports start via NGL, what is that price going to look like then? Double? Triple? And if Europe is forced to buy gas via LNG exports, what happens then to domestic pricing?

North America is not an island of resources as long as there remains a global marketplace. Of course if that changes we won’t have to worry about the cost of energy as no one will be working, anyway. We live by trading and we die by it. In an energy constrained world with a functioning marketplace the playing fields level over time as regards to energy. Asian slave-like labour rates still the biggest advantage going forward.

paulo

MSN Fanboy on Sat, 30th Aug 2014 12:22 pm

If he gets his wish, where will the profit for the oil / gas companies arise from?

The happy chappy operates a financial fund,comes up with a tapestry of graphs…

AND COMPLETLY MISSES THE POINT.

Yet again, another delusional fool: who is in control of your money.

Our species… sigh.

Nony on Sat, 30th Aug 2014 3:16 pm

Really good article. The Marcellus is mighty. 16 BCF/day at sub $3 wellhead price. And growing. And that’s with less than 100 rigs.

http://www.eia.gov/petroleum/drilling/pdf/marcellus.pdf

And you have the Utica coming on now, too.

keith on Sat, 30th Aug 2014 8:02 pm

You also have interest rates rising in summer 2015? Shale recovery companies will go bust, if it happens 2013-14 revenues 570 billion, expenses 670 billion, reported by EIA. Ponzi scheme.

Makati1 on Sat, 30th Aug 2014 8:20 pm

MSN, you are correct. This was not even worth reading. I certainly wouldn’t use their findings as a basis to ‘invest’, or should I say, gamble, in the Market Casino.

Norm on Sun, 31st Aug 2014 5:22 am

Where is the peak oil website? To what domain has it moved to? This is an economic Fed money stimulus Volcker Ben Bernanke money supply website. Nothing about oil here.

Boat on Sun, 31st Aug 2014 8:02 am

Norm, plenty of oil for at least a decade so we are in a holding pattern waiting for the collapse after that.

MSN Fanboy on Sun, 31st Aug 2014 9:35 am

Norm: the reason we speak of finance is simple, peak oil isn’t just geology… otherwise 2008 would have been the peak, with no shale to fill the gap.

Finance matters, as it represents cost and most importantly profit.

It also asks at what price can people pay?

When over 50% of the population can’t afford one car for financial reasons, peak oil will be here.

Its, how do i put it, between a rock and a hard place. Thus, between geology and Finance lies peak oil.

jjhman on Sun, 31st Aug 2014 7:18 pm

What?

I must have fallen asleep reading the financial prognostications of a fund manager who can’t beat the S&P 500 index and who seems to miss the point that some hundreds (or thousands)of bankers were breaking the law when they made “liar loans”. No,he wants to blame excessive regulations. And, of course, St. Ronald saved the economy by reducing taxes and regulation. Maybe running the largest govt deficit in history (up to that point) helped too.

I’m pretty sick of hearing these financial types whine about “regulations”. They never seem to be able to list a specific regulation that affected them. Maybe its the ones about not stealing other people’s money.

Makati1 on Sun, 31st Aug 2014 7:57 pm

jjhman, maybe it is the simple one:

“Thou shalt not steal!”

8th Commandment. We now have over 300,000 laws in the US but the original 10 were sufficient. Problem is, that doesn’t support 1,000,000+ lawyers in the manner they prefer.

Boat on Mon, 1st Sep 2014 8:57 am

paulo, nat gas consumption grew in the US over 6%., Mexico consumption of nat gas is growing fast also. Yet natgas is at $4. Down to 400 drilling rigs from 1600 or so. Higher prices would create yet another explosion of drilling rigs and continued expansion. The talk of peak nat gas is decades away.

longtimber on Mon, 1st Sep 2014 9:52 am

Who needs Nat Gas? Future Transport fuel source

breakthrough at the end of the Aug 29th episode of http://evtv.me

FrAncisca on Mon, 26th Oct 2015 5:07 am

, I would like to show you, Jesse, that Skull and Bone created Hurricane Katrina with state owned egaetroctinemlc weaponry; as they do all weather now. I can show you with a date and time when I disclosed this publicly, causing them to stall the hurricane heading to Cuba; at which time was being reported to be slammed. When the stall ended and the hurricane weapon reactivated it continued its path towards Cuba, but only brushed it with little to no damage or destruction. Elated for Cuba, but unfortunately, I couldn’t find a person of conscience in the U.S. to stop it from slamming into New Orleans. It is my reporting, disclosing of Skull and Bones egaetroctinemlc weather weaponry that has prevented them from further attacking and targeting Florida, incognito, with their so-called hurricanes. As well, I can show the same date and time evidence that caused them to stop erupting Mt. St. Helen public disclosure of their crimes, incognito, is what stops and prevents them from committing them. Members of Skull and Bone are, in a word, EVIL, without conscience and will stop at nothing to get what they want, even to their own demise; that is, after they take everyone else with them. Obama better shake the spider webs from his head and issue arrest warrants for them ASAP. They are radiating us, I have proof in my fingernails, and plastic that was made malleable both in my yard and house, they have put something in our tap water now, since the first extreme cold/freezing tempuratures, that causes my hands to become dry and chafed, literally splitting open the skin drawing blood, my hands look like an 80 year olds hands, I’m 53. Since I’ve determined this to be the problem, yesterday, I quit putting my hands in the water and it’s clearing up with the help of some hand repair aloe cream, and will have to use bottled water to brush my teeth and wash my face, but I need a shower, wash my hair and I’m afraid to do so, of the results. I will be contacting the water company today, but they’ve lied to me before, and they just put in all new pipes in this section to replace the old ones they said were not a problem causing rusty water. I’ve had these people poison my food coming from restaurants here, one that is owned by the family of a friend of one of my nephew’s who is a New York City cop, I’ve had them do things to food I buy at the grocery stores, I’m afraid to eat anymore. I was surprised to find out Obama’s connection to the CIA, I knew there was some connection, nothing in Washington happens by accident, but they are riding shotgun all over him, out of control, or else he wants to see me dead too. Life around her is like a daily shoot out at the OK Corral, kill or be killed, well, I’m still shooting, waiting for one of my bullets to hit them square between the eyes, stop them cold, DEAD! And as usual, the reinforcements are flying over head when I’m disclosing something they don’t want exposed, right on que. One more thing, now that I have their attention, I heard their loud, uproarious egaetroctinemlc weaponry tonight at the Cobblestone Store Plaza between 9-10pm, the same loud, uproarious egaetroctinemlc weaponry I heard from my house and forced the police to enforce the noise ordience to get rid of them a few years back now. Let’s talk Jesse, these EVIL Lunatics must be stopped and eliminated ASAP!

http://www.url2go.online/mikewick.com on Mon, 7th Dec 2015 5:24 am

That’s a shrewd answer to a tricky question

Lore on Thu, 15th Nov 2018 2:36 am

No more s***. All posts of this qulaity from now on