Peak Oil is You

Donate Bitcoins ;-) or Paypal :-)

Page added on May 9, 2017

Measuring Energy Return on Investment at a National Level

A recently published study proposes a novel approach to measure how much ‘net energy’ is produced at national level.

François-Xavier Chevallerau | April 25, 2017

Economic growth requires energy. Or rather, it requires ‘net energy’, i.e. energy effectively available to do other things than procuring, processing and distributing energy. A growing body of research suggests that the increasing availability of net energy has played a key role in driving economic growth since the beginning of the Industrial Revolution. This net energy has historically been obtained from energy resources that have tended to deliver significantly more usable energy to society than the amount of energy that has had to be expended to obtain it, namely fossil fuels, and most particularly oil. However, concerns are mounting that the net energy gain of conventional fossil fuels is declining over time as resources get depleted, decrease in quality and get more difficult to obtain, while alternatives such as unconventional fossil fuels (e.g. shale/tight oil and gas), nuclear, bio-fuels or renewable energy sources tend to have lower net energy ratios.

As societies and economies transition away from high net energy resources such as conventional fossil fuels and towards lower net energy resources such as unconventional fossil fuels or renewables, either voluntarily (e.g. to fight climate change) or due to resource constraints, a rising share of the total energy supply has to be dedicated to finding, harnessing, transforming and conveying energy to meet a growing demand. The share that can be made available for other uses (i.e. the net to society) therefore tends to decrease, constraining ‘discretionary’ investments and consumption. This net energy decrease appears to be only partly offset by technology-enabled efficiency gains, and the supply of energy available for doing other things than getting energy is thus becoming increasingly constrained over time, eroding potential economic growth and the ability to continue delivering improvements in social wellbeing.

A metric often used to measure the net energy ratio of various types of energy resources is the ‘energy return on (energy) invested’ (abbreviated EROI or EROEI) i.e. the ratio between the total amount of energy delivered by an energy resource and the amount of energy invested in obtaining and delivering it. The higher the EROI of an energy resource, the ‘cheaper’ it is in energy terms, and the more ‘valuable’ it is in terms of producing (economically) useful energy output. Numerous EROI analyses have been conducted over the last few years, which present a picture of the potential contribution of individual energy sources to the energetic needs of the economy. However, less attention has so far been paid to determining aggregate EROI values at national level. Doing so indeed requires a different methodological approach to traditional EROI analyses, due to the mix of particular resource locations, exploitation times and technologies applied to ‘produce’ energy, i.e., to extract fossil fuels and capture flows of renewable energy in a given national territory.

A recent study by British reserachers aims to address the conceptual and methodological gap in relation to calculating a national-level EROI and analysing its policy implications:

Developing an Input-Output Based Method to Estimate a National-Level Energy Return on Investment (EROI)

Energies 2017, 10(4), 534. Published: 14 April 2017

Lina I. Brand-Correa, Paul E. Brockway, Claire L. Copeland, Timothy J. Foxon, Anne Owen, and Peter G. Taylor

The study identifies three key reasons why determining a national-level EROI is important:

- EROI gives a better picture of resource depletion and accessibility than traditional energy analyses (i.e., mainstream energy-economic analyses that are widely used for decision-making purposes) and is therefore relevant for energy-economy analysis and national energy planning;

- EROI can provide valuable information about the relative resource depletion and technological change in resource extraction/capture when measured over time in a given country to take account of dynamic effects, thus providing net energy analysis and insights at the same (national) scale as that required by policy-makers;

- EROI can help understand the potential for growth or change of a national economy in relation to the physical energy cost of extracting/capturing the energy it requires.

The study therefore aims to contribute to developing a method for measuring EROI for national economies. To this end, it combines three aspects of net energy analysis (NEA) at a country level that have been left aside or pursued separately in previous attempts at measuring aggregate EROI levels:

- accounting for international energy trade (both direct and embodied) in the calculation of indirect energy investment;

- using data for a more than one year; and

- taking a national perspective.

A key hurdle for measuring national-level EROI consists in properly calculating indirect energy investment and in allocating indirect energy use from different stages of the supply chain to the country’s various energy producing sectors. To do so the study uses an Input-Output (IO) methodology to track all indirect energy investment requirements of the national energy sector. Physical flows are estimated from monetary economic data, which is based on an economic transactions matrix (a table where all inter-industry transactions within a year are recorded in monetary terms) combined with an energy extension vector (which contains the amount of energy used by each industry in energy units). This makes it possible to allocate energy sales and purchases to every industry, and then track down the paths that lead to the energy industry itself by quantifying interrelationships across economic sectors and even attributing embodied energy inputs to traded goods and services. In a globalised economy, the indirect energy flows used by a national energy sector in order to extract/capture energy can also originate overseas, and calculating a national-level indirect energy investment therefore requires accounting for energy trade (both direct and embodied). To do so, the study uses Multi-Regional Input-Output (MRIO) data from various sources.

Like many other energy analysis techniques, energy IO analysis was developed in the 1970s in the wake of the oil price shock. It has been mainly been used since then to quantify energy flows through the different economic sectors, but it has not been used so far to directly calculate an empirically-based national-level EROI value using an MRIO modelling approach. The study therefore develops a novel application of what is a well-established methodology in the field of emissions accounting.

Using this methodology, the study calculates the national-level EROI for the UK for the period 1997–2012. It finds that this EROI increased from 12.7 in 1997 to a maximum of 13.8 in 2000, before gradually falling down to 5.6 in 2012. This means that for every unit of energy the UK energy extracting/capture sectors have invested, they have obtained an average of 10.2 units of energy during the period 1997-2012. In other words, on average, 9.8% of the UK’s extracted/captured energy does not go into the economy or into society for productive or well-being purposes, but rather needs to be reinvested by the energy sectors to produce more energy.

National-level EROI for the UK, 1997-2012: comparison of results with and without indirect energy (EiE).

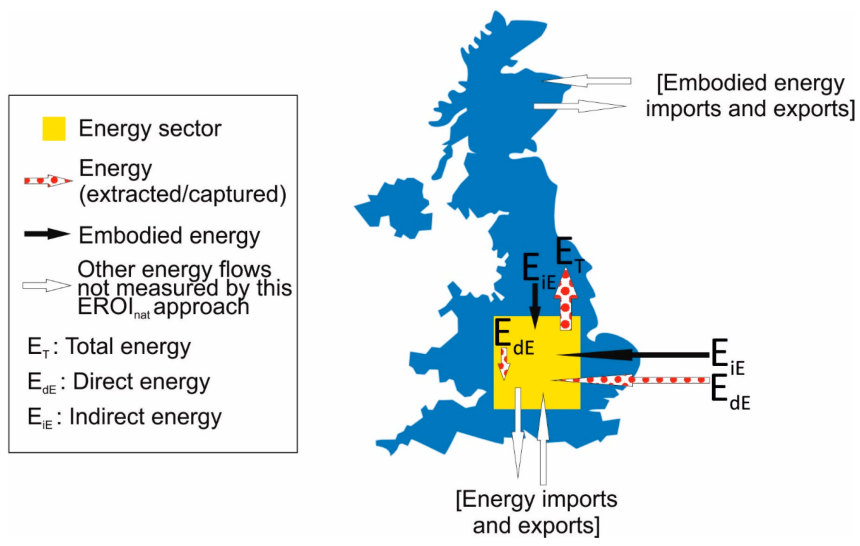

It should be noted that the study aims to measure the ‘energy return’ of national energy production, rather than of national energy use. The system boundary for the EROI analysis is thus established at the resource extraction/capture level, rather than further down the energy chain to include downstream transformation processes. The analysis focuses on the energy extracted/captured in a country (energy returned), regardless of how and where this energy is then used, i.e. whether it is transformed and consumed in the country or rather exported. Therefore, it does include energy exports but excludes energy imports, meaning that it is only applicable to a country where energy is effectively extracted/captured, and that a country that imports all of its primary energy would not have an EROI value when using this methodology. A consumption-based EROI calculation, accounting for energy imports and including more processing and transformation stages further down the energy chain might give very different figures and information.

National-level EROI – UK case. Black and dotted arrows represent what is measured, while white arrows represent flows that occur but are not included in this approach to national-level EROI given its boundary of analysis.

The first stage of extraction/capture of energy sources has been chosen in this case, as it provides a well-defined starting point for a novel methodology that can be further built upon. The proposed method can in fact provide a long-term dynamic view of the evolution of a national-level EROI from an ‘energy production’ perspective. In the case of the UK, the drop of the national-level EROI from 2003 onwards reflects the steady decline of the country’s production of energy since 1999, which has been compensated by increased imports that do not enter in the calculation. For the national-level EROI from a production perspective, this means that the UK’s energy sector is extracting/capturing less energy while using a relatively stable stream of energy inputs. Considering that oil and gas dominate the UK’s energy production mix, the decline of the national-level EROI is also likely to reflect the evolutions of the EROI values of these particular fuels as well as the evolution of their proportion in the national energy production. The method used however cannot provide information concerning the timing of energy inputs and energy outputs for specific energy sources. These inputs and outputs can vary significantly over the functional life of an energy supply technology, since energy inputs are typically high at the beginning (construction) and at the end (decommissioning) of the life of the energy extraction or capture location, while energy outputs are maximum in between, once the technologies are fully deployed and operational. A massive investment in renewable energy technologies such as solar and wind, for example, would be likely to push down the national-level EROI in the short term, while longer time-series would be required to assess its overall long-term effect. The results of the study, as they stand, do not yet provide much insight into the effect of a transition to renewables from a national-level EROI perspective.

Despite these limitations, the study’s findings have important implications for the energy sector, for resource management and technology development, and for the economy. The study’s proposed methodology for national-level EROI calculation has the potential to inform national as well as international energy policies. Once developed further, for more countries and over more years, the results may help answer important questions such as:

- Which countries are extracting and capturing energy with a better return to their energy invested?

- Which countries are doing better in terms of technological development and/or resource conservation?

- How do national EROI values for different countries relate to their energy imports and exports?

Above all, the relevance of a national-level EROI lies in its potential to inform policy decisions that aim to manage an energy transition to a low carbon economy. In general, countries should aim to have high levels of national-level EROI, since this means that more net energy is available for use in the productive economy. Decreasing levels of national-level EROI are to be expected for countries investing heavily in renewables to address climate change, but this trend should be closely monitored by policy-makers in order to ensure that, as renewable energy capture technologies improve, the national-level EROI trend also picks up. Even if the EROI values of renewables may increase in the future from current relatively low values, policy makers also need to better understand what a transition to renewable energy sources would imply for our economies and societies, and the measurement of national-level EROI values can help them to do so.

Biophysical Economics Policy Center

13 Comments on "Measuring Energy Return on Investment at a National Level"

Wildbourgman on Tue, 9th May 2017 2:17 pm

I don’t know if this has been talked about here or if it’s even something that can be easily quantified, but I’d like to know how much oil could I have bought with the entire amount of money that was invested in shale plays in the last ten years. I know that the price you use makes a big difference, but I’m curious at what price would it be profitable as per EROEI.

Wildbourgman on Tue, 9th May 2017 2:19 pm

Oh and that’s how much oil one could have bought versus the amount that’s projected to be produced if we stopped drilling and spending in those shale fields today. Yeah I know that’s a tough one.

Dave Thompson on Tue, 9th May 2017 5:23 pm

EROEI is an educated guess. The tell is apparent when looking at long term GDP. Charles A. S. Hall has written mostly being ignored and points out the trend of GDP over the decades. GDP is dropping over time and can be tracked with the conclusion being we are screwed.

peakyeast on Tue, 9th May 2017 6:26 pm

I hate it when people abuse definitions.

EROI is NOT EROEI and no amount of brackets can make up for that.

In this case I suppose abbreviating François-Xavier Chevallerau to just ASS is also valid.

KW/h or is not $ or £. Although there is a relationship.

All types of energy is not equal – so at least the EROI should be a range or a specificed energy mix to purchase – not a just a definite number. – Depending on what energy (mix) you want to buy to use for the extraction.

Jout / $in is not Jout / Jin.

dave thompson on Tue, 9th May 2017 9:48 pm

EROI AND EROEI are inter changeable if you do not understand the biophysical world we live in and only go by econ 101 stats you will never get it peakyeast.

rockman on Tue, 9th May 2017 10:06 pm

Wildman – “I’m curious at what price would it be profitable as per EROEI.” Actually I think they just gave you the answer. Of course you understand it’s not just the oil price per se but the economic analysis which also takes into account the cost to develop those reserves at $X/bbl.

And you may remember one of the many (so many f*cking times, LOL) times I estimated the minimum EROEI (or EROI if you prefer) that would be economic to drill. And son of a bitch…it’s in the same range that they estimated how low it got in England: around 5 to 6. Look closely at their curve and though not perfect it does a good job of being INVERSELY proportional to oil prices. And that’s because (as you know so well) no decision to drill a well has ever been, isn’t being today, and never will be based upon the energy returned. Those decisions are based on the $’s returned and not the bbls returned. IOW on the potential rate of return. And let’s not forget how many grossly overestimate how much energy it takes to drill and complete a well…usually less the 10% of the total well cost.

Which, in general terms and subject to the price of oil, means it’s difficult to ECONOMICALLY justify drilling a well if it doesn’t produce at least 5 to 6 times the energy the Btu’s it takes to drill. But more specifically if it doesn’t produce 5 to 6 times the VALUE of the energy produced. Which is why high oil prices allow lower energy returns because those returns are worth more $’s. Conversely when oil prices fall dramatically it takes more bbls returned to generate more $’s returned. IOW that minimum 5 to 6 range would represent a time of high oil prices…like we had a few years ago. Which is exactly how the industry was able to develop plays (like the shales) which have a tendency to recover smaller volumes of oil from less attractive prospects.

And when oil prices are low it takes more bbls returned to generate the same justifiable ROR’s as when oil prices were high. Yes: as a result of lower oil prices wells currently being drilled have a higher energy return then they did several years ago. Which means only the better prospects are being drilled. And that’s being proven by the better initial flow rates of today’s wells.

Lower oil prices = more bbls ($’s) produced = higher energy returns.

So again just a rough estimate but I would guess returns have increased from 5-6 to 10-12.

Wildbourgman on Wed, 10th May 2017 7:04 am

Ok Rockman that’s a pretty good explanation.

I’m thinking about starting an oil company. The first thing I’m going to do is wait for a mania to erupt and then find investors and/or banks to loan me some start up funds. Then I’m going to give myself (the CEO) a nice bonus because I was able to accomplish the goal of getting start up funds.

After that it’s all good. Oil or no oil, profitability or loss, I really don’t care at that point.

CIA-MOLE on Wed, 10th May 2017 8:03 am

Why do people insist on talking about EROI when it’s money that dominates everything?

If money goes into electric cars then that’s where I’ll invest, not oil companies.

GregT on Wed, 10th May 2017 9:32 am

Fiat money is a claim on future production. (Debt) Production requires energy. Money does not manufacture electric cars, energy does.

rockman on Wed, 10th May 2017 3:29 pm

Wildman – “Then I’m going to give myself (the CEO) a nice bonus because I was able to accomplish the goal of getting start up funds.” The reality: for every person I’ve known personally who got stinking rich finding oil/NG profitably I’ve know at least 3 that did it by gaming the system just as you described. In the 80’s I consulted for a small pubco where the president (a former stock broke) came back from NYC just laughing his ass off over the smucks (as he called them) that gave him $500k for some warrants that he wouldn’t only not deliver $1 of the interest but never return $1 of principal. Lost control of the company when it filed bankruptcy. But he had already transfered $millions to overseas accounts. I could have burned him but couldn’t just make any public claims without documentation without getting sued by him. But if someone filed a suite against him I could unload under oath at no risk to myself. But I could not get one group to file against him. Most were brokers that didn’t care to have their clients learn what a crook thier advisers had gotten them in bed with.

And then in the early 90’s hooked up with another small start up public. I’ll skip the details but just another pack of crooks. But one detail: they did a $1O0 million. And how close did the brokerage houses that placed the bonds scrutinized the company? They collect $14 million in commission. After that no more working for such companies. Just consulted until I finally hooked up with my current gig with a privately owned company. IOW when someone is investing their only money there’s not much incentive to steal any of it. LOL.

Working with small oil pubcos is like the old joke: if you watch someone make sausage you might never eat another link. Same thing by watching from the inside the inner workings of such companies. Big companies can play similar games but when you’re down towards the base of the employee pyramid you don’t get to see it.

rockman on Wed, 10th May 2017 3:44 pm

CIA – “If money goes into electric cars then that’s where I’ll invest, not oil companies.” Had you invested $76,000 in Chevron stock in August 2015 you could have sold it for 56% more just 16 months later: $118,000 in December 2016. And been paid almost 5% in dividends while you held it.

Historically oil companies stocks make much investments after a bust when the industry is in the toilet then during a boom time. Not rocket science: buy low…sell high. LOL.

Jerome Purtzer on Wed, 10th May 2017 6:42 pm

Wild and Rock, do not invest in Oil Wells or Electric Cars. Invest in printing presses to produce the cash. Simple. The Government has been doing it for years and I guess it will work until someone wakes up. Looks like you already had some brushes with Brokers, Bankers and Crooks, Rock.

rockman on Wed, 10th May 2017 10:57 pm

Jerome – Believe or not in 41 years I didn’t invest $1 in the oil biz. Other people’s money? Oh, hell yes. LOL.